Multi-Entity Consolidation Software: What Finance Teams Should Evaluate First

Buying multi-entity consolidation software? Evaluate entity structure, COA mapping, FX, intercompany workflows, and reporting fit first.

Executive summary

- Start with structure: Map how consolidation works before comparing tools.

- Check entity fit: The system must match your legal, management, and reporting views.

- Test COA mapping: Different charts of accounts create most of the hidden work.

- Review intercompany early: The hard part is not the elimination entry. It is the review before it.

- Control FX logic: Rate treatment needs ownership, consistency, and traceability.

- Track adjustments: Top-side entries should not live as unexplained spreadsheet fixes.

- Use real outputs: Test the tool against your actual board pack, not the vendor demo.

The consolidation file says group revenue is $4.8m.

The entity-level reports say $5.3m.

Both numbers came from finance.

That gap is usually where the search for multi-entity consolidation software begins. A CFO sees too many versions of the same number, too many manual checks, and too much dependency on one person who understands the spreadsheet.

The mistake is evaluating tools by asking, “Can it consolidate multiple entities?”

Most can, at least in a clean demo. The better question is whether the system fits the way your group actually closes, reviews, adjusts, and reports.

For multi-entity finance teams, the messy part is not the final consolidated P&L. It is everything that happens before it.

Why multi-entity consolidation software should start with workflow, not features

A feature checklist feels useful. It gives the team something to compare.

But consolidation rarely breaks because a tool lacks a “consolidate” button.

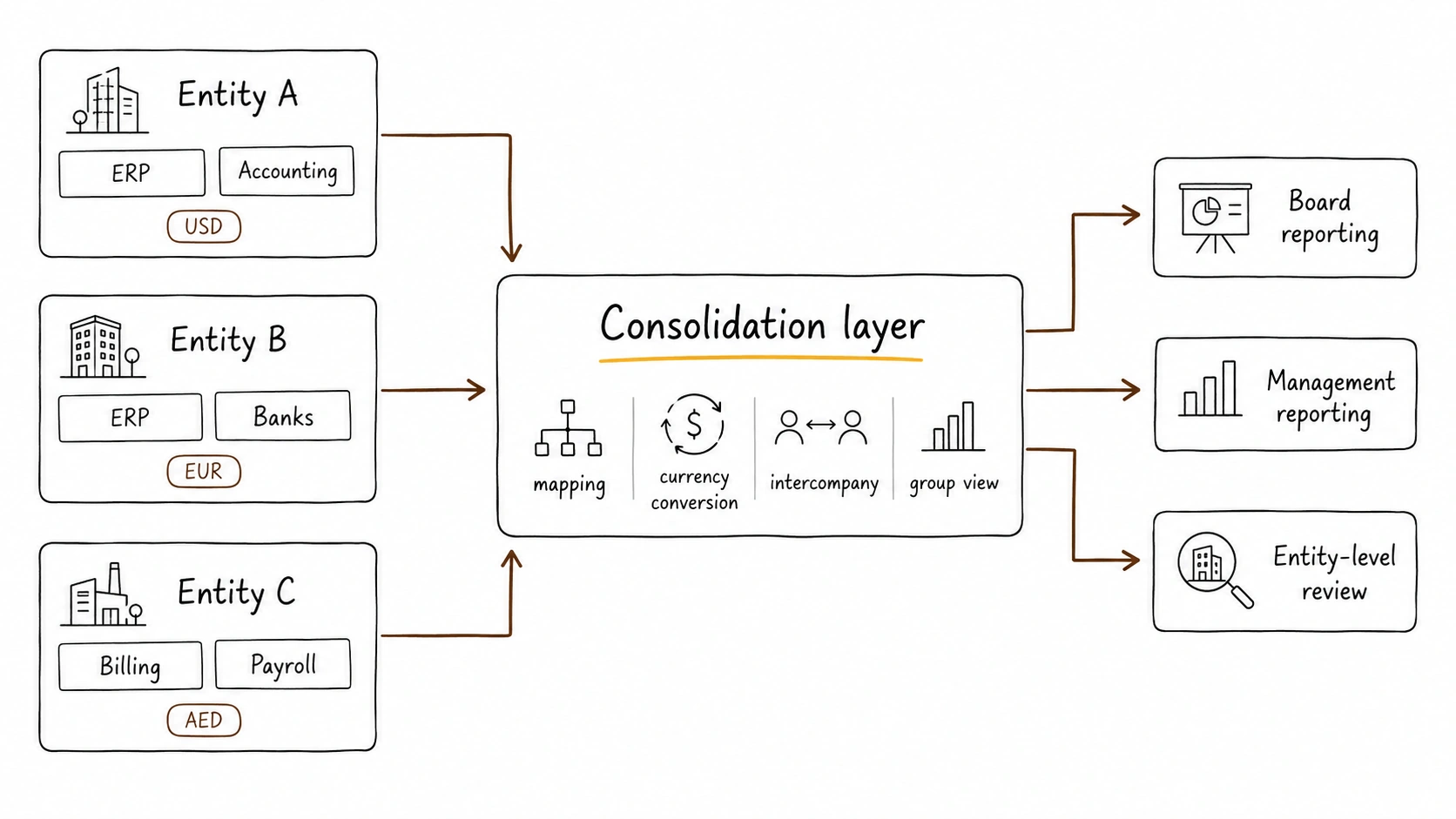

It breaks because the business has different entities using different systems, currencies, account structures, and reporting views.

A UAE holding company may have a Saudi operating entity, a free zone entity, and an acquired subsidiary. One entity may use Wafeq. Another may use a local ERP. A smaller entity may still send Excel exports. The group may report in USD while local books run in AED or SAR.

That is the real buying context.

Before reviewing vendors, finance should answer five questions:

- Which entities need full consolidation?

- Which entities only need reporting visibility?

- Which systems does each entity use?

- Which currencies and FX rules apply?

- Which reports does leadership actually rely on?

If those answers are unclear, the buying process becomes superficial. The team ends up comparing dashboards before understanding the operating model underneath them.

How multi-entity consolidation software should handle chart of accounts mapping

Chart of accounts mapping creates more consolidation pain than most teams expect.

One entity records software revenue under “Sales.”

Another uses “Subscription Income.”

A third puts implementation fees under “Other Revenue.”

None of these labels may be wrong locally. But at group level, they create noise.

Good multi-entity consolidation software should let finance map local accounts to group reporting lines without losing the local detail. It should also show unmapped accounts, track mapping changes, and make recurring logic easy to review.

This is where spreadsheets start to fail.

At first, the mapping file works because one person understands it. Then a new entity gets added. Then the group changes reporting lines. Then someone edits a lookup formula. The file still produces a number, but finance loses confidence in the route behind it.

For a deeper explanation of why the reporting layer matters before the tool choice, see Alternatives to Fathom, Syft, and Causal for Multi-Entity Finance.

We've also written about how some companies opt to use PowerBI dashboards instead of newer tools, and that has its own context into how it relates to multi-entity consolidation efficiency.

Intercompany review is the real test of multi-entity consolidation software

Most teams ask whether the software can eliminate intercompany balances.

That question comes too late.

The harder question is whether the system helps finance review intercompany activity before elimination.

For example:

Entity A records a management fee. Entity B records the matching expense one month later. One side reports in AED. The other reports in SAR. The descriptions do not match. The balances do not tie cleanly.

The final elimination entry may still make the consolidated report look correct. But the process behind it carries risk.

Finance needs to identify related-party balances, match counterparties, review timing differences, separate FX noise from true mismatches, and approve the treatment before the group view goes out.

If all of that happens in Excel, the close becomes dependent on memory and manual judgment. That may work for two entities. It becomes fragile at five.

For more on the mechanics behind this issue, read What Are Intercompany Eliminations? The Math Behind Ghost Revenue.

FX and adjustments need traceability

Multi-currency consolidation is not just a conversion problem.

It is an ownership problem.

Who controls the rates? Which rate applies to P&L accounts? Which rate applies to balance sheet accounts? How are historical rates handled? Can finance explain how FX affected the reported result?

When rate logic sits in offline files, small changes create large questions. Prior months can shift. Variances become harder to explain. The CFO sees movement but cannot quickly separate business performance from currency impact.

The same issue applies to top-side adjustments.

Every consolidation process has them. Some correct timing issues. Some reclass costs. Some align management reporting. The problem is not the existence of adjustments. The problem is when they become spreadsheet fixes with weak explanations.

A proper system should show what changed, which entity it affected, who made the change, why it was made, who reviewed it, and whether it reverses next month.

Without that trail, finance may still produce the report. But audit, board review, and due diligence become harder than they need to be.

When spreadsheets break

Spreadsheets do not break suddenly. They break in stages.

First, one person owns the file and knows how to avoid mistakes. Then a new entity gets added. Then intercompany balances take longer to reconcile. Then FX treatment creates recurring questions. Then top-side adjustments sit outside the source systems. Then leadership starts waiting for finance before making hiring, cash, or spending decisions.

That is the moment where manual consolidation stops being a finance inconvenience and becomes an operating constraint.

The issue is not that spreadsheets are bad. They are useful for analysis and review. But they are weak as the control layer for recurring multi-entity consolidation.

A system becomes necessary when the business needs repeatability, traceability, and faster review across entities.

The practical buying checklist

Before buying multi-entity consolidation software, finance should pressure-test the tool against these questions:

- Can it support both legal entity reporting and management reporting?

- Can it work across mixed accounting systems?

- Can finance control the chart of accounts mapping without technical help every month?

- Can it support intercompany review before elimination?

- Can it handle AED, SAR, USD, and other reporting currencies with clear rate logic?

- Can it track top-side adjustments with ownership and approval?

- Can it reproduce the actual board pack without a final Excel rebuild?

- Can users trace group numbers back to entity-level detail?

The final test is simple: take last month’s board pack and ask whether the system can recreate it with less manual work and a better audit trail.

Do not test the vendor’s ideal report. Test your real one.

This is also why entity-level visibility matters. A clean group number can still hide risk inside one subsidiary. The Flagship Illusion is useful context on how group totals can mask operating problems.

The final evaluation question

Do not ask only:

“Can this software consolidate our entities?”

Ask:

“Can this system support how our finance team needs to consolidate, review, explain, and report across entities every month?”

That question changes the buying process.

It moves the discussion away from generic dashboards and toward operating fit.

Kudwa’s multi-entity consolidation software supports consolidation across fragmented systems, entities, currencies, intercompany activity, and chart-of-accounts mapping. But finance teams should still evaluate it against their own close workflow, entity structure, and reporting outputs.

No system removes the need for finance judgment.

The right system removes the manual work that makes that judgment slow, inconsistent, and hard to trace.

Book a walkthrough to see how Kudwa supports multi-entity consolidation across fragmented finance systems: Book a demo

Latest from Kudwa

KSA Company Compliance Obligations: What Finance Teams Should Track in the First 90 Days

Track KSA company compliance obligations in the first 90 days, from ZATCA and payroll to audit readiness, AI reminders, and owner review.

Flux Analysis vs Variance Analysis: What GCC Finance Teams Actually Need

Flux analysis vs variance analysis matters because close review and management reporting answer different finance questions.