Flux Analysis vs Variance Analysis: What GCC Finance Teams Actually Need

Flux analysis vs variance analysis matters because close review and management reporting answer different finance questions.

Executive summary

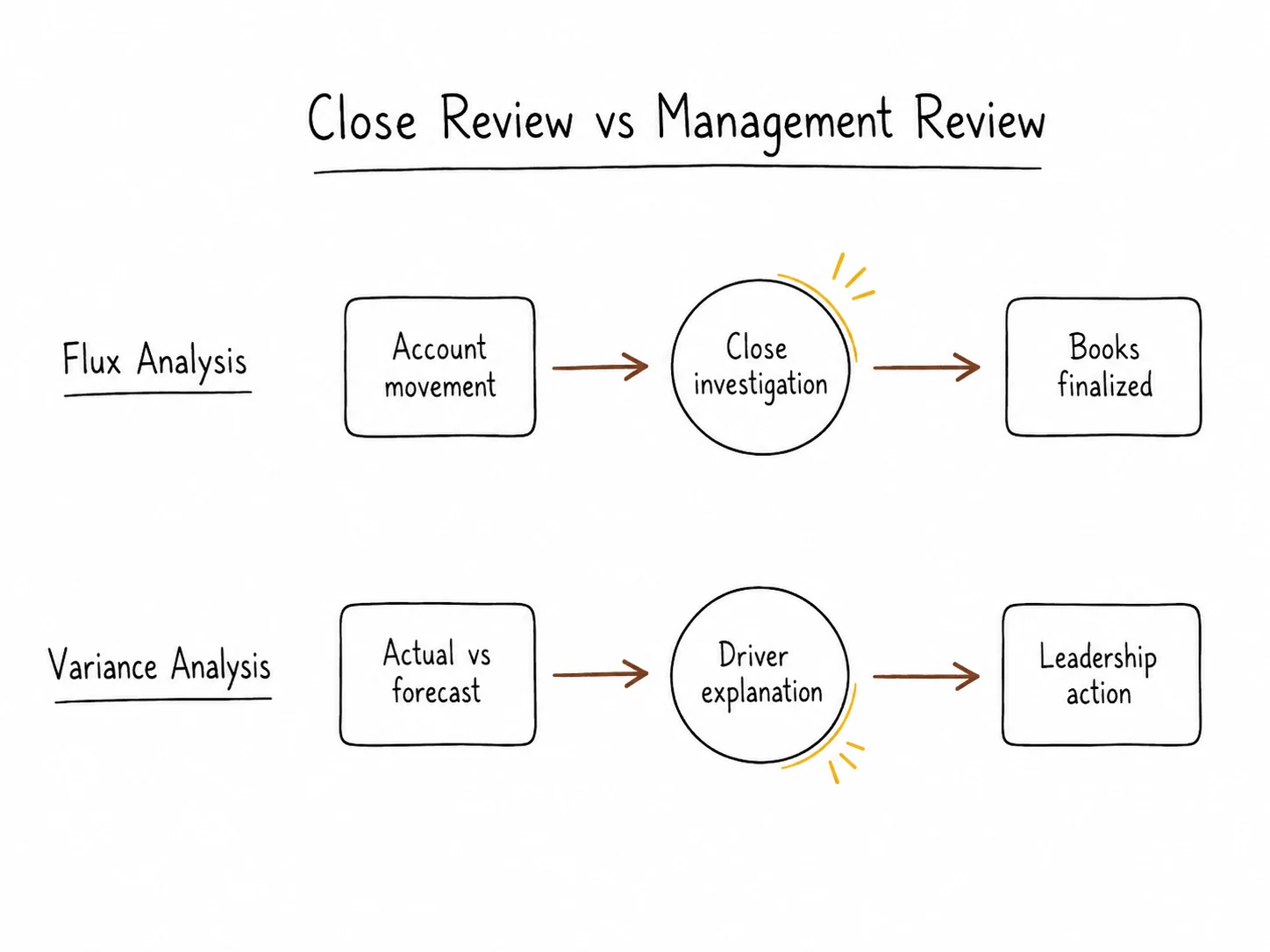

- Flux analysis explains account movement during close; variance analysis explains performance against plan after close.

- Close teams use flux to check postings, cutoffs, accruals, and classifications before books are finalized.

- FP&A and finance leaders use variance analysis to explain drivers, forecast impact, cash movement, and management action.

- Multi-entity GCC teams need both workflows, but they should not expect one layer to do the other’s job.

Why the terms get confused during close

It is Day 5 of close. Payroll expense is up 18% from last month, and the finance team is reviewing the movement. One person asks whether the flux has been explained. Another asks whether this is why EBITDA missed forecast.

Both questions are reasonable, but they belong to different workflows.

Flux analysis vs variance analysis gets confusing because both compare numbers. Flux analysis asks whether an account moved as expected during close. Variance analysis asks why actual performance differed from forecast, budget, or plan after close.

For GCC finance teams, the distinction matters once the business has multiple entities, currencies, departments, and reporting layers. Accounting may confirm the ledger movement is correct, while leadership still needs to know whether UAE margin declined, KSA revenue beat plan, or cash moved differently from EBITDA.

What flux analysis means

Flux analysis is a close-stage review of account movement. It usually compares the current period against a prior period and asks whether the movement is expected, supported, and properly classified.

Take rent expense. It increased from AED 120,000 last month to AED 185,000 this month. The close reviewer checks whether a new lease started, a prepaid adjustment was posted, rent was duplicated, or a prior accrual reversed. The goal is not to explain company performance yet. The goal is to decide whether the account balance is reasonable before close is finalized.

Flux analysis is usually owned by accounting, controllership, or the close team. It belongs close to the accounting system, ERP, close management tool, or account reconciliation workflow. It helps finance close with control, but it does not create the management explanation a CFO needs for leadership reporting.

What variance analysis means

Variance analysis is a post-close management review. It compares actuals against forecast, budget, plan, or operating expectation and asks why performance differed.

The same payroll movement looks different here. Payroll may be up 18% month-on-month, but the management question is whether payroll was above forecast because hiring happened earlier than planned, bonuses were accrued, sales headcount shifted from UAE to KSA, contractor costs moved into payroll, or allocations changed.

That is not only an accounting question. It needs closed actuals, forecast assumptions, department ownership, entity context, operating drivers, and commentary. This is why forecast vs actual reporting matters as a separate workflow. A close review can confirm payroll was posted correctly; variance analysis explains whether that number changes the hiring plan, EBITDA outlook, cash runway, or department-level view.

Flux analysis vs variance analysis: practical comparison

The mistake is expecting one workflow to do the other’s job. A close tool can identify unusual account movement, but it may not know the forecast assumption, department owner, cash consequence, or board narrative. A reporting layer can explain performance, but it should not replace the controls needed to close and reconcile the books.

Why GCC multi-entity teams need the post-close view

For a small single-entity business, flux and variance can feel close together because the same person may close the books and explain the result. In a GCC group, the gap becomes clearer.

Revenue might beat forecast in KSA but miss in UAE. At the ledger level, revenue movement may look reasonable. At the management level, the issue could be country mix, delayed collections, project timing, or the difference between bookings and recognized revenue.

Cash creates the sharper example. EBITDA may improve while cash declines because collections lagged, supplier payments cleared early, payroll timing shifted, VAT payments landed in the month, or one entity funded another. Flux analysis can explain account movement. It does not automatically explain group liquidity.

This is where the granularity gap appears. Leadership rarely needs only the total movement. It needs the entity, department, account, cash, and driver-level explanation behind the movement. The same issue appears in multi-entity consolidation software, where a consolidated number can look stable while one entity carries the pressure.

Where each belongs in the stack

Flux belongs close to accounting and close. The right layer is usually the accounting system, ERP, close management tool, or account reconciliation workflow.

Variance belongs closer to management reporting and FP&A. It needs actuals, but also forecast assumptions, department structures, entity views, cash context, and operating drivers. The goal is not only to confirm that a movement happened. The goal is to explain what it means.

Kudwa fits in that post-close layer. It is not trying to replace the close workflow or accounting system. It helps finance teams move from closed numbers to management-ready explanations by connecting actuals, forecast assumptions, operational drivers, entity structures, currency views, and commentary inside a controlled reporting and analysis workflow.

Flux helps finance close the books. Variance helps leadership understand performance. Multi-entity GCC teams need both, but they should not expect one workflow to do the other’s job.

If your team can explain account movements during close but still struggles to explain performance across entities, departments, cash, and forecast drivers after close, the gap is likely post-accounting. See how Kudwa helps connect closed actuals to finance analysis and forecasting, or book a demo.

Latest from Kudwa

Finance KPI Reporting: Why Leadership Teams Disagree on the Same Number

Finance KPI reporting needs controlled definitions, source data, calculation logic, and cadence so leaders stop debating versions of the same metric.

Reporting Software for Finance Leaders: What to Actually Look For

Reporting software for finance leaders should help explain, trace, and defend numbers, not only format dashboards and board packs.