Cash Flow Forecasting vs Cash Flow Management: Why a Polished Model Cannot Fix Weak Visibility

Confusing cash flow forecasting vs cash flow management leads to cash surprises and delayed operational decisions. Learn the operational differences.

Executive Summary

- Operational distinction: Forecasting is a time-bound projection of future liquidity; management is the continuous operational control of positions, timing, and variance.

- Failure mechanism: Cash models break when teams use recognized accounting revenue instead of granular, behavior-adjusted collection dates.

- Complexity trap: Multi-currency and multi-entity timing misalignments quickly turn stable group-level forecasts into local cash crunches.

- Spreadsheet limits: Mixing current bank balances with manual forecast assumptions creates a stale operating view within forty-eight hours of an update.

- System trigger: Software becomes necessary when the finance team spends more hours manually reconciling cash movements than analyzing why actuals deviated from the model.

The Q3 hiring plan was approved because the forecast showed a comfortable six-month runway. Two weeks later, finance had to freeze the roles. Collections slipped, payroll cleared three days earlier than expected, and the cash model had pulled recognized revenue instead of actual cash receipts.

The formulas in the spreadsheet weren't mathematically broken. The problem was an operational conflation: the finance team had mistaken cash flow forecasting for cash flow management.

Cash Flow Forecasting vs Cash Flow Management: The Operational Boundary

To manage cash effectively, a finance team must separate projection from execution. Treating them as the same process is how companies with strong P&Ls end up in liquidity traps.

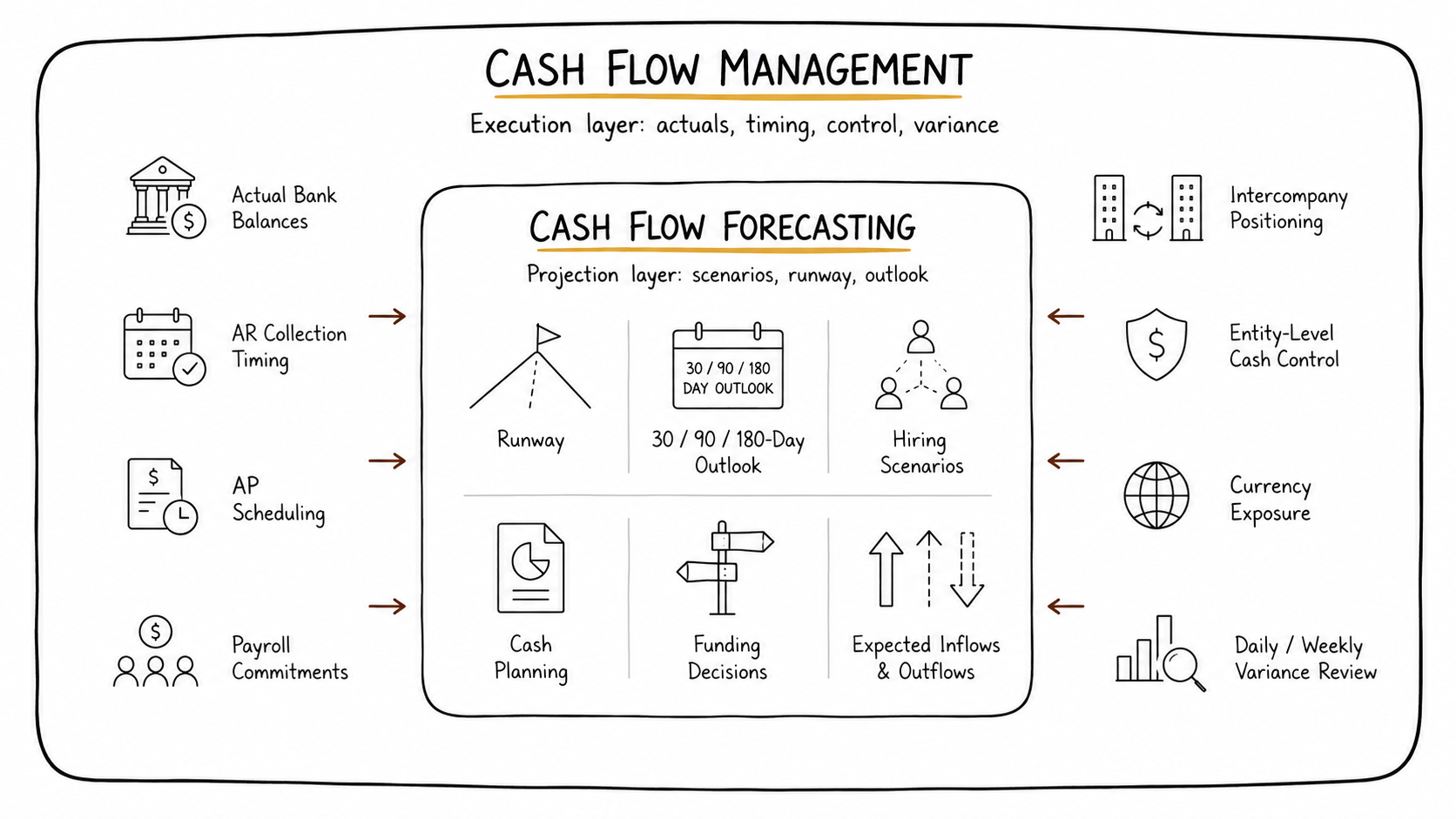

- Cash flow forecasting is a design exercise. It looks forward, aggregating historical trends, sales pipelines, and scheduled expenses to estimate where the business will stand in 30, 90, or 180 days. It answers strategic leadership questions about runway, investment capacity, and funding requirements.

- Cash flow management is the operational control layer. It monitors real-time bank balances, enforces accounts receivable (AR) collection workflows, schedules accounts payable (AP) runs, handles multi-entity positioning, and reviews daily variances.

A forecast built without tight cash management is just an isolated spreadsheet model. It tells you where you might land, but gives you no levers to control the journey.

The Specific Mechanism of Failure

Consider a business generating $500,000 in monthly recognized revenue.

The finance team builds a cash forecast that assumes this $500,000 arrives evenly across the month. Based on this projection, leadership approves a $350,000 cash outlay for payroll and vendor payments on the 25th.

Here is how the operating reality breaks down:

- Recognized Revenue: $500,000

- Actual Expected Collections (based on true AR aging): $280,000

- Committed Outflows (Payroll + Suppliers): $350,000

- Real-time Cash Deficit: -$70,000

The model did not fail because the math was wrong. It failed because it used the wrong operating layer. It substituted accounting definitions for cash reality, ignoring customer payment behavior, weekend clearing delays, and actual payment terms.

Unpredictable cash timing is a primary reason what is the biggest financial risk for companies shifts from a theoretical conversation to an immediate operational crisis.

Where Complexity Destroys the Spreadsheet Model

For a single-entity business with consistent subscription revenue, a basic spreadsheet model can survive. But as a company scales past $1M+ in revenue, complexity introduces friction that manual sheets cannot handle.

1. The Multi-Entity and Multi-Currency Timing Gap

Group-level consolidated forecasts often mask severe localized cash shortages. For example, a parent company in the UAE might invoice in AED and see healthy consolidated cash on paper. Meanwhile, its Saudi Arabian subsidiary collects in SAR but faces localized delays due to withholding tax filings or regional bank clearing cycles.

If a USD-denominated supplier payment hits the parent bank before those SAR funds can be converted and concentrated, the group faces a localized liquidity crunch. A monthly consolidated forecast completely misses this intra-month currency and entity exposure.

2. Disconnected Operating Schedules

A cash forecast becomes unreliable the moment its inputs live on different update schedules.

- The bank balance is pulled on Monday morning.

- The AR aging schedule is exported on Tuesday afternoon.

- The AP run is modified on Thursday during a vendor negotiation.

- The payroll file is finalized on Friday.

When these components are updated asynchronously across manual tabs, the finance team spends its time fixing broken data links rather than evaluating variance. This operational strain shows how lean finance teams can run serious reporting without adding headcount only when they fix the underlying data flow instead of hiring more analysts to copy and paste numbers.

The Cash Operations Decision Tree

Visual here:

This framework helps determine whether your current finance stack requires a better projection model, tighter operational controls, or a dedicated data layer.

Moving From Static Projections to Real-Time Control

To fix the disconnect between cash flow forecasting vs cash flow management, finance teams must separate their actual cash position from their forecast assumptions. A stronger operating model requires three specific shifts.

1. Separate Cash Actuals from Theoretical Forecasts

Do not maintain actual bank positions and forecast movements in the same manual matrix. The actuals should serve as an unalterable baseline, pulled directly from your ERP and banking portals. The forecast should sit as a flexible overlay that applies probability weights to your collections and payments based on historical operational performance.

2. Move from Monthly to Rolling Weekly Views

A monthly cash view is too blunt an instrument for managing working capital. A business can be net-positive over a 30-day period but technically insolvent on day 14. High-velocity finance operations require a 13-week rolling cash mechanism, where every week's variance is reviewed before the next payment run is cleared.

3. Establish a Connected Post-Accounting Layer

When a finance team tries to solve this problem by replacing their ERP or accounting software, they often create a multi-month implementation project that fails to solve the underlying cash visibility problem. The accounting system is designed to record historical transactions, not to model future cash positioning across fragmented bank accounts and regional subsidiaries.

This is where a post-accounting layer such as Kudwa can help: not by replacing your accounting software, but by connecting bank, accounting, entity, and reporting data into an integrated cash flow management view. This approach allows finance leaders to run reliable financial analysis and forecasting without manual data manipulation.

Understanding what a unified financial data platform actually replaces in a growing finance stack helps teams avoid the trap of expensive, long-term ERP overhauls when the immediate requirement is simple, reliable data connection.

What a Finance Director Must Check Before Upgrading

Before buying software or rebuilding the cash model, review four parts of the current process.

AR input quality

If the forecast uses invoice due dates as if they were cash receipt dates, the model is too optimistic. A stronger process adjusts expected collections using actual payment behavior, such as customer tier, collection patterns, and real DSO slippage.

Data recency

If bank balances and ledger data are exported manually once a week, the team is working off a stale baseline. A stronger setup gives finance daily visibility into bank and ledger movement so the forecast starts from a current position.

Variance cadence

If variance review only happens during month-end close, the team is reacting too late. A stronger process reviews actual vs. forecast movement weekly, ideally before supplier runs, payroll, or major cash commitments are executed.

Entity isolation

If intercompany transfers are mixed together with external collections and operating inflows, the group cash view becomes distorted. A stronger process separates intercompany funding loops from true cash generation so finance can see where liquidity is actually coming from and where it is being consumed.

The Practical Takeaway

If your finance team is spending more time updating cells than reviewing cash allocation, you are not managing cash—you are maintaining a spreadsheet. A reliable cash forecast is the result of a structured cash management process. Address the operational layer first; the model will follow.

See how Kudwa helps finance teams connect cash visibility, reporting, and forecast assumptions across their existing systems. Learn more about Kudwa’s cash flow management layer.

Latest from Kudwa

What Governed AI Actually Means in Finance

Governed AI in finance means outputs stay traceable to source data, finance rules, permissions, and review before decisions are made.

KSA E-Invoicing Timeline: ZATCA Fatoora Deadlines and Finance Readiness Checklist

Track the KSA e-invoicing timeline, ZATCA Phase 2 waves, Fatoora integration, and finance readiness checks for Saudi companies.