What a Unified Financial Data Platform Actually Replaces in a Growing Finance Stack

A unified financial data platform replaces the fragile spreadsheet layer finance rebuilds across ERP, CRM, banks, payroll, and reporting.

Executive summary

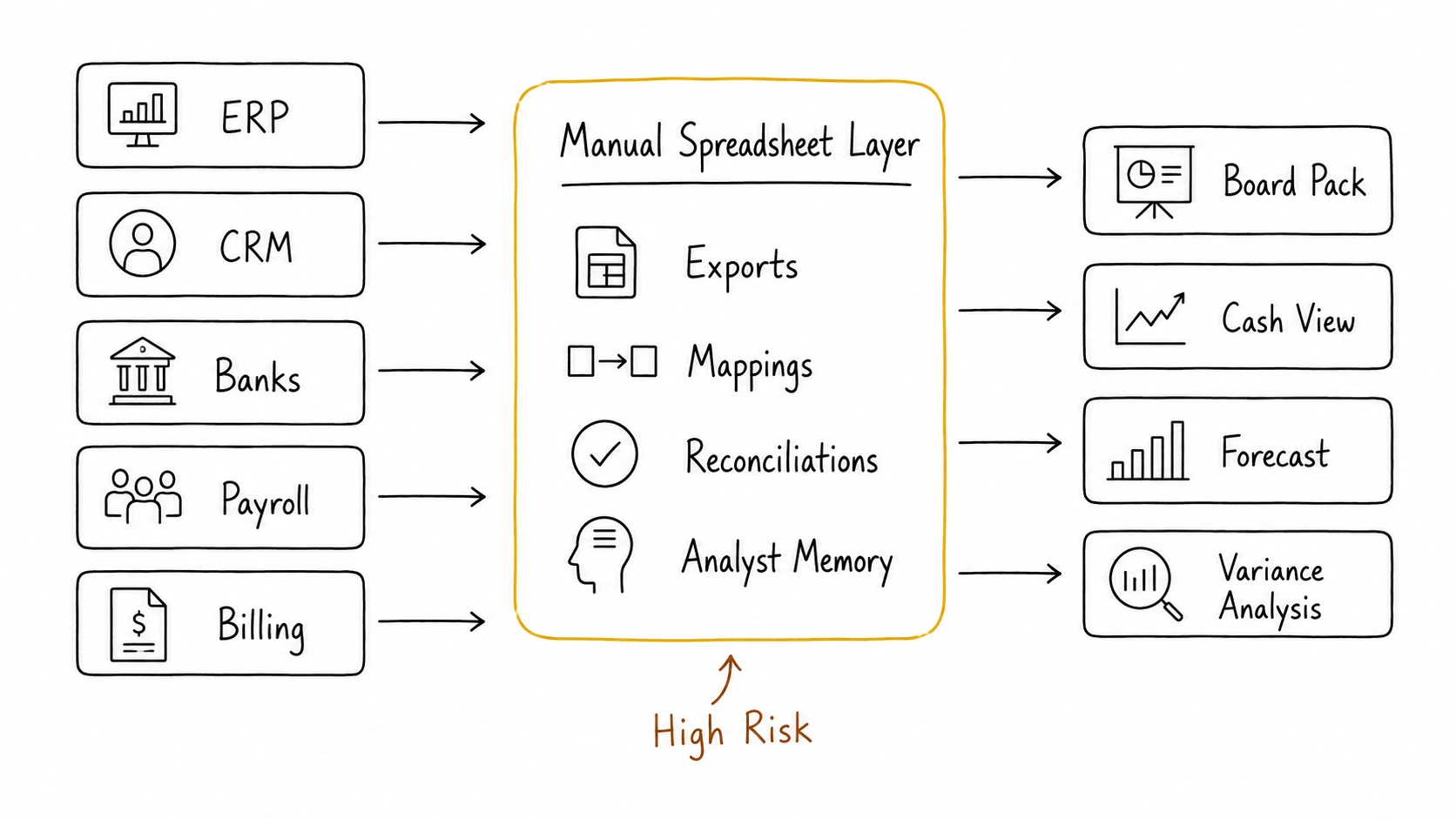

- Manual layer: Most finance teams already have a unified financial data platform. It lives in exports, mappings, and workbooks.

- Real problem: The issue is not that data sits in different systems. The issue is that finance has no controlled layer between those systems and the decisions they support.

- Hidden risk: One workbook often carries consolidation, cash visibility, reporting logic, and metric definitions at the same time.

- GCC pressure: Multi-entity and multi-currency operations across AED, SAR, and USD make fragmentation show up earlier.

- Breaking point: Spreadsheets break when finance uses them as recurring infrastructure instead of flexible analysis tools.

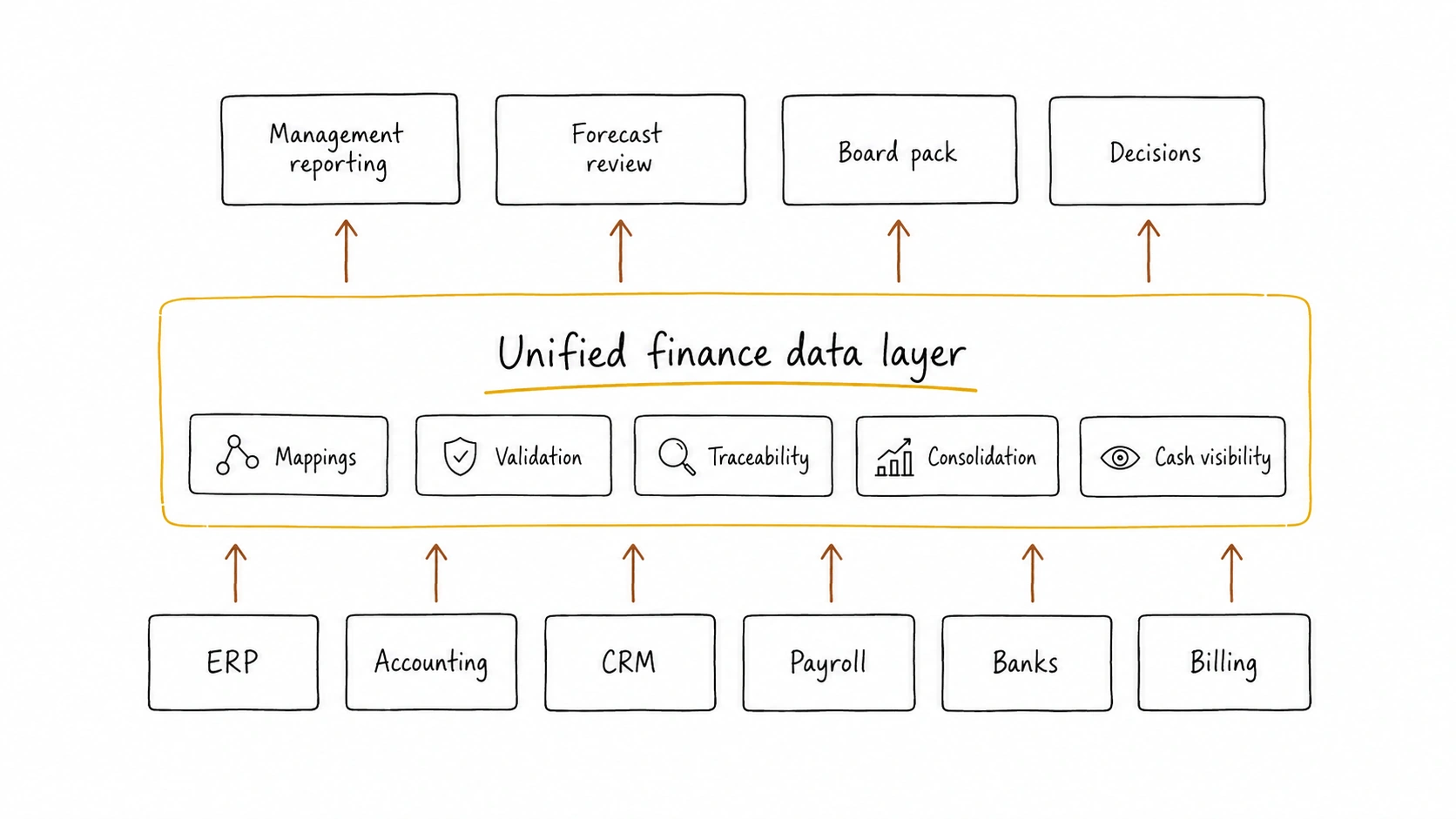

- Right role: A unified layer should not replace source systems. It should standardize what comes out of them.

- Decision test: The core question is not whether the company needs another tool. It is where finance data becomes decision-ready.

“We have AED 4.2M in cash.”

That answer may be true.

The UAE bank portal says one thing. The Saudi entity’s accounting file says another. USD collections sit in Stripe. Payroll has not hit yet. Two supplier payments cleared after the last export. The group cash report still shows last Thursday’s position.

So the number is true in one system and wrong for the decision.

That is the operating problem behind a unified financial data platform. It is not a category finance teams need to learn from scratch. Most growing teams already build one manually every month. They export from the ERP, pull bank balances, clean CRM data, map payroll, rebuild entity views, update a consolidation workbook, and send a reporting pack. Then leadership asks for the same view by region, product, entity, department, and cash impact.

The platform already exists. The question is whether it sits in a controlled finance layer or inside a fragile spreadsheet.

What a unified financial data platform replaces

A unified financial data platform replaces the manual stitching layer between the systems finance already uses.

It does not replace the ERP. It does not replace accounting software. It does not replace the CRM, payroll tool, bank portal, billing system, or forecast model. Those systems still have jobs to do. The ERP should own the ledger. The CRM should own pipeline and sales activity. Payroll should own employee cost inputs. Banks should own actual cash movement.

The unified layer replaces the recurring work finance does after those systems produce data: monthly CSV exports, spreadsheet mappings, offline cash trackers, copy-paste reporting packs, and the analyst memory that explains which formula, exception, or adjustment matters this month.

This distinction matters. If a CFO hears “platform” and thinks “new system migration,” the conversation goes in the wrong direction. The job is not to rip out the finance stack. The job is to remove the uncontrolled layer finance built around it.

For many teams, this becomes a post-accounting layer such as Kudwa: a layer above the systems of record that helps finance standardize fragmented data, consolidate results, and produce management reporting without replacing the tools already in place.

Why a unified financial data platform becomes necessary

A company can run on separate tools for a long time when the operating model stays simple. One entity. One currency. One accounting system. One main bank. One clean revenue model. In that setup, finance can usually keep the reporting model under control with disciplined spreadsheets and a tight close process.

Complexity changes the math. Not because the team gets worse. Because the number of relationships between systems grows faster than the number of systems.

A five-system finance stack does not create five reporting problems. It can create dozens. CRM owns customer names, sales regions, pipeline, and deal owners. Billing owns invoices, collections status, failed payments, and revenue timing. Accounting owns recognized revenue, expenses, payables, and trial balances. Banks own actual cash movement. Payroll owns people cost, departments, benefits, and timing. Spreadsheets own budget assumptions, allocations, and board reporting.

Each system may work correctly on its own. The problem starts when leadership asks a cross-system question.

“Why did cash fall even though revenue grew?”

That answer needs invoiced revenue, collected cash, AR aging, supplier payments, payroll timing, bank movement, revenue recognition, FX impact, and forecast assumptions. No single source system answers that cleanly. So finance builds the answer manually.

This is the same problem explored in Kudwa’s article on why more tools can create less financial clarity. Tool count is not the issue by itself. The issue is the absence of a common layer that standardizes what those tools produce.

The manual finance platform most teams already run

Here is the real month-end workflow in many growing companies.

Finance exports trial balances from accounting systems, pulls AR and AP detail, downloads bank balances, refreshes CRM or billing reports, copies payroll summaries into the model, updates entity and department mappings, reconciles mismatches, builds consolidated views, writes variance commentary, moves charts into a reporting pack, and answers follow-up questions when leadership asks for a different cut.

The official stack may look clean on a slide: ERP, CRM, payroll, banking, and BI. The real operating stack looks different:

Source systems → exports → spreadsheet logic → manual checks → reporting pack → follow-up analysis

That middle section carries the risk. It is where definitions change, files go stale, mappings drift, and one person’s memory becomes part of the reporting process.

Spreadsheets do not fail because they are weak tools. They fail when finance asks them to become infrastructure. A spreadsheet can support analysis, scenario testing, and one-off modeling. It should not carry the recurring burden of being the company’s consolidation layer, cash visibility layer, reporting layer, and metric definition layer at the same time.

Where manual processes break

Manual finance processes usually break in three places: timing, definitions, and ownership.

Timing breaks first. Reports depend on data that changes after finance exports it. A cash report pulled Monday morning may miss payments that cleared Monday afternoon. AR aging may change after collections updates. Payroll accruals may arrive after the first management pack draft. CRM bookings may shift after sales operations cleans the pipeline. Finance can still produce the report, but the report becomes stale faster.

Definitions break next. Sales may define revenue by booked deals. Accounting may define it by recognized revenue. Operations may define it by delivered service. Cash may show collections net of timing. None of those teams are necessarily wrong. They answer different questions. The problem starts when leadership sees one “revenue” number without knowing which definition they are looking at.

Ownership breaks last, and it creates the most risk. Only one analyst understands the consolidation workbook. The finance manager reviews formulas instead of performance. Every close depends on last month’s file. Nobody wants to change mappings because they fear breaking the pack. Leadership questions create new workbook versions. At that stage, the spreadsheet has stopped supporting finance. It has become part of the control environment.

What the unified layer actually has to control

A unified layer should solve four operating problems.

1. Structure

Finance needs common definitions across systems. The same customer may appear as “ABC Trading LLC” in the CRM, “ABC Trading” in accounting, and “ABC UAE” in a collections tracker. That looks small until revenue, AR, collections, and customer profitability need to line up.

The same applies to accounts, departments, entities, products, projects, regions, vendors, employees, and currencies. A unified layer needs clear mapping logic for each one. Without that structure, reporting becomes translation work.

2. Traceability

Finance should trace a reported number back to source detail. If the board pack says group revenue grew 18%, the team should know which entities, customers, products, and timing movements drove it.

A spreadsheet can support this for a while. But once finance starts copying values across tabs, exporting static files, and adjusting numbers outside source systems, traceability weakens. The reporting pack may still look polished. The audit trail behind it gets thinner.

3. Repeatability

A monthly process should not depend on someone remembering every manual step. Finance will always need flexible analysis. The problem starts when recurring reporting depends on the right export sequence, the right file naming convention, the right hidden mapping tab, the right manual FX rate, and the right person knowing which exception to ignore.

That is not a process. It is institutional memory.

4. Decision readiness

A unified financial data platform should shorten the distance between the number and the decision. Leadership does not only need the P&L. They need the answer behind the P&L.

What moved? Where did it move? Why did it move? Was it timing, margin, volume, pricing, FX, hiring, collections, or one-off spend? A dashboard can show the variance. Finance still needs the structured data behind it to explain the variance.

A simple test works here:

Finance data readiness = structure + traceability + repeatability + decision context

If one of those pieces is missing, finance may still report the number. It will struggle to explain it quickly.

GCC example: three entities before the finance team catches up

Take a company with three GCC entities.

The UAE parent, KSA subsidiary, and holding company all use the same cloud accounting system. On paper, that sounds controlled. Finance has one vendor, one familiar ledger structure, and one standard place to pull accounting reports.

At month-end, the manual process still looks manageable. Export each entity’s P&L. Translate balances into the group reporting currency. Map local account usage into the group reporting structure. Combine cash by bank and currency. Review entity performance. Explain revenue, margin, operating expenses, and cash movement.

Then normal operating reality gets involved.

The UAE entity records a management fee to KSA on April 30. KSA books the expense on May 2. The holding company sends USD funding to the UAE parent. Payroll sits in a separate file. Bank data sits outside the accounting system. The CRM tracks sales region, but accounting tracks legal entity. Department owners use different cost-center logic across entities.

The board does not only want a consolidated P&L. It wants to know which geography drove the margin change, which department caused the cost movement, where cash actually sits, and whether the variance came from operations, FX, timing, or intercompany activity.

This is where the issue becomes clearer.

The problem is not always that each entity uses different software. Many companies standardize on one accounting system and still struggle to produce a unified finance view. The gap sits between recorded accounting data and decision-ready reporting.

A simple consolidated P&L is no longer enough. Finance needs a consistent group reporting model that can explain performance across entities, currencies, departments, cash positions, and operating dimensions.

This is where the topic extends into multi-entity management reporting. The issue is not only consolidation. It is whether finance can move leadership from group performance to entity-level exceptions, cash movement, variance drivers, and decisions without rebuilding the story manually every month.

When a unified financial data platform becomes necessary

A unified financial data platform becomes necessary when finance can no longer control recurring reporting through effort alone.

It is probably premature if one accounting system holds most finance data, the company has one entity and one main currency, leadership asks for the same basic reports each month, mappings rarely change, and cash visibility comes from one or two sources.

It becomes necessary when finance exports from multiple systems every month, rebuilds the consolidated view from scratch, explains why different teams quote different numbers, manually updates entity and department mappings, tracks cash across portals and spreadsheets, and loses time preparing data before analysis can start.

The trigger is not company size. The trigger is recurring data friction.

A $1M revenue company with one entity and a simple model may not need a unified layer. A $5M revenue company with three entities, multiple currencies, and a lean finance team may need one badly. Headcount follows complexity. Reporting pain often arrives before headcount.

For a deeper breakdown of how close complexity changes as entity count grows, the 1 vs 3 vs 5 entity close framework is the natural next read.

What the unified layer should not replace

A unified financial data platform should not become a second ERP. That mistake creates more confusion.

The ERP or accounting system should still own the ledger. The CRM should still own the sales process. Payroll should still own employee cost inputs. Banks should still own actual cash movement. Billing should still own invoice and payment mechanics.

The unified layer should own the finance view across those systems. That means the reporting chart of accounts, group mappings, department logic, cash visibility structure, intercompany visibility, management reporting, variance analysis, and finance definitions across systems.

The goal is not one system for everything. The goal is one controlled layer for the finance questions that require data from many systems. This is also why product pages such as Data in One Place should not be read as “put every process into one tool.” The sharper interpretation is: give finance one trusted place to connect, standardize, and trace the data it already depends on.

The better operating question

Do not start with: “Do we need another platform?”

Start with: “Where does our finance data become decision-ready?”

If the answer is “inside the ERP,” the current stack may still work. If the answer is “inside a spreadsheet that only one person understands,” the company already has a platform. It just has a fragile one.

A unified financial data platform replaces that fragility with structure. It gives finance a cleaner way to move from source systems to reporting, from reporting to explanation, and from explanation to decisions.

Spreadsheets still have a role. They remain useful for ad hoc analysis and scenario work. They should not carry the recurring burden of consolidation, cash visibility, reporting logic, and metric definitions all at once.

That is where growing finance stacks usually fail. Not because the tools are bad. Because nobody owns the layer between them.

See how the Kudwa platform connects existing finance systems into a cleaner layer for reporting, consolidation, and analysis.

Latest from Kudwa

KSA Company Compliance Obligations: What Finance Teams Should Track in the First 90 Days

Track KSA company compliance obligations in the first 90 days, from ZATCA and payroll to audit readiness, AI reminders, and owner review.

Flux Analysis vs Variance Analysis: What GCC Finance Teams Actually Need

Flux analysis vs variance analysis matters because close review and management reporting answer different finance questions.