Financial Close Process for Multiple Entities: The 1 vs 3 vs 5 Breakdown

See how the financial close process changes from 1 to 3 to 5 entities, and why larger groups become exponentially harder to manage.

The Close Does Not Scale in a Straight Line

It is Day 7 of the close.

The parent company books are finalized. Entity two is waiting on an intercompany reconciliation. Entity three exported a trial balance in SAR that does not map cleanly to the group chart of accounts.

Three spreadsheets are open. The consolidated board view is still days away.

This is where finance teams realize that closing multiple entities is not just a larger version of closing one entity.

A financial close process for multiple entities does not scale in a straight line. One entity does not become three times harder at three entities and five times harder at five. The work compounds.

Every new entity can add another chart of accounts, another currency, another close calendar, another system, another intercompany relationship, and another reconciliation layer before leadership can trust the group view.

A single-entity close is about completing one ledger accurately. A multi-entity close is about aligning several ledgers into one reliable group picture.

That is a different operating problem.

Why Multi-Entity Close Complexity Compounds

A single-entity close has clean assumptions: one chart of accounts, one functional currency, one accounting system, one ledger, and one reporting calendar.

The process can run sequentially: reconcile accounts, post accruals, review the trial balance, prepare reporting, and explain variances.

That model starts to break when more entities are added.

By three entities, finance usually starts dealing with manual mapping, different account structures, timing mismatches, and intercompany reconciliation.

By five entities, the issue becomes structural. The team is not just doing more close tasks. It is managing a matrix of ledgers, currencies, systems, intercompany relationships, and reporting dependencies.

The real shift is not only the number of entities. It's the number of relationships finance has to control before the group view can be trusted, and entity count is only the first layer. Once departments, cost centers, currencies, and reporting dimensions are added, finance is no longer managing a list of entities. It is managing a reporting matrix.

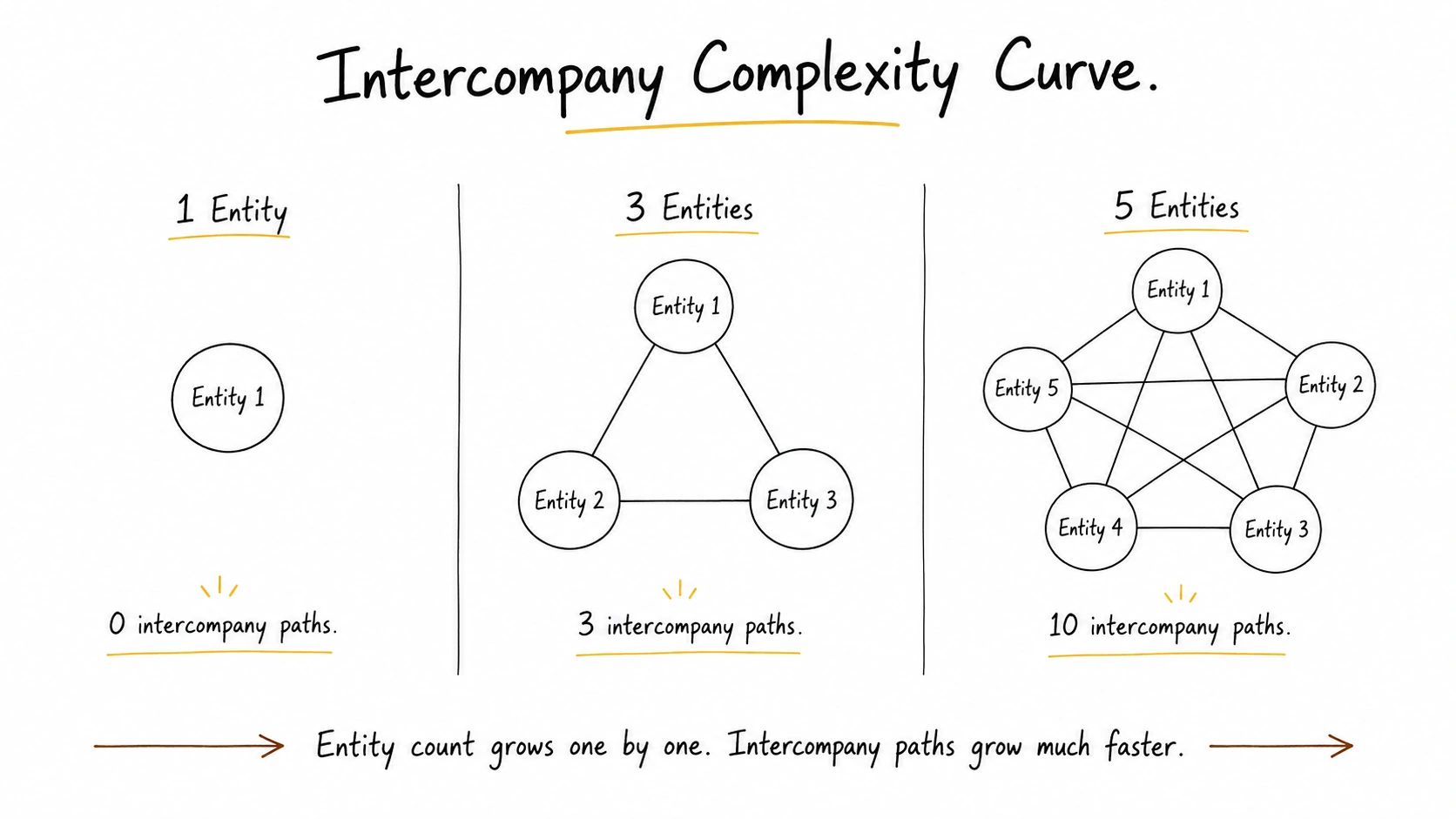

The 1 vs 3 vs 5 Breakdown

1 Entity

Close structure: Sequential ledger close

Typical close time: 3–5 days

Headcount needed: 1–2 finance team members

Intercompany paths: 0

Primary failure point: Accrual accuracy

With one entity, finance is mainly checking whether the ledger is complete and accurate. The risks are familiar: late invoices, missed accruals, unreconciled accounts, payroll adjustments, and variance explanations.

The workflow is mostly linear. A spreadsheet-supported process can still work if transaction volume is manageable.

3 Entities

Close structure: Sequential close plus manual data merging

Typical close time: 8–12 days

Headcount needed: 2–3 finance team members

Intercompany paths: 3

Primary failure point: Chart of accounts mapping

At three entities, the close becomes more than a ledger exercise.

Finance has to align different trial balances, check account mappings, and make sure entity-level results roll up into one reporting structure. The parent company may close on time, but the consolidated view waits for subsidiary data, mapping adjustments, intercompany checks, and manual spreadsheet work.

This is often where the group close starts to slow down.

5 Entities

Close structure: Parallel close plus matrix reconciliation

Typical close time: 15+ days without stronger systems or process discipline

Headcount needed: 4+ finance team members, or a leaner team absorbing delays

Intercompany paths: 10

Primary failure point: Intercompany eliminations

At five entities, finance is no longer merging a few ledgers.

The team is managing parallel closes across multiple entities, each with its own inputs, account structures, currencies, and timing risks.

If each entity can transact with the others, five entities create ten possible intercompany paths. That means more balances to match, more recharges to confirm, more shared costs to track, and more eliminations to review before the group numbers are ready.

This is where manual consolidation becomes the bottleneck.

Beyond Five Entities: Departments Multiply the Close

Five entities is not the ceiling. It is the point where the pattern becomes obvious.

At ten entities, finance is not managing ten isolated closes. If every entity can transact with the others, there are 45 possible intercompany paths. At fifteen entities, there are 105.

That is before adding departments.

A group with 10 entities and 5 departments in each entity is not just a 10-company close. It is 50 reporting slices before finance even starts comparing performance across departments, entities, currencies, and reporting lines.

The finance team may need to answer questions like:

- Which department drove the margin decline in Saudi?

- Did the UAE marketing cost increase come from one entity or several?

- Are shared technology costs allocated consistently across all entities?

- Is the same department coded the same way in every chart of accounts?

- Which department-level variances are real, and which are mapping issues?

This is where close complexity becomes exponential.

The team is no longer only consolidating legal entities. It is consolidating legal entities, departments, currencies, accounts, systems, and reporting dimensions into one group view.

That is why larger companies can have strong accounting systems and still struggle with group reporting. The issue is not the absence of ledgers. The issue is the number of relationships between them.

The Three Bottlenecks That Break the Close

The jump from one entity to three introduces new work. The jump from three entities to five changes the operating model. Beyond that, departments and reporting dimensions multiply the number of views finance has to reconcile.

Most breakdowns appear in three places.

1. Chart of Accounts Drift

As entities grow, they often develop their own local accounting logic.

One entity may classify software costs under IT expenses. Another may split them between subscriptions, cloud infrastructure, and capitalized implementation costs. A third may use a local accounting system with its own structure.

That may work locally, but it creates problems at group level.

A group close needs a standard way to map local accounts into a common reporting structure. Without that, finance spends too much of the close manually reclassifying trial balances instead of reviewing performance.

For GCC businesses, this is common. A UAE parent may use one setup, a Saudi entity may use software configured around local compliance needs, and another regional entity may use a legacy ERP.

The issue is not that any one system is wrong. The issue is that the group needs a common reporting layer above them.

2. Intercompany Mismatches

Intercompany mismatches become more painful as entity count grows.

The problem is not one transaction. It is the repeated need to check whether every internal balance, recharge, loan, shared cost, or management fee has been recorded properly on both sides.

For example, Entity A in the UAE pays for a $10,000 group software license. Entity B in Saudi Arabia should absorb part of the cost. Entity C in Oman uses the same license but receives the recharge one month later.

If each entity records the transaction differently, the group view becomes harder to trust. One entity may show inflated costs. Another may show understated expenses. The consolidated pack may require manual corrections before leadership can review it.

This is why intercompany should not be treated as a late clean-up task. In a strong multi-entity financial close process, intercompany checks happen before consolidation begins.

3. FX and Fragmented Systems

Multi-entity groups often operate across several currencies and systems.

A GCC structure may involve AED, SAR, OMR, QAR, USD, or other currencies. Each entity may also run on a different accounting setup, ERP, billing tool, payroll system, or banking structure.

This creates two problems.

First, finance has to translate balances correctly. Balance sheet accounts, income statement accounts, equity accounts, intercompany balances, and historical balances may not use the same rates.

Second, finance has to collect and standardize data from different systems before reporting can begin.

When this work is handled in spreadsheets, formula errors, stale rates, manual exports, and inconsistent assumptions can enter the close. Even when the team catches the issue later, the delay affects reporting speed and confidence.

When the Consolidation Workbook Becomes the Bottleneck

Excel can work for a simple group.

It starts to break when finance uses it as the main consolidation layer across multiple entities, currencies, and systems.

The warning signs are clear:

- trial balances are exported manually every month

- entity mappings are adjusted by hand

- intercompany eliminations depend on linked spreadsheets

- FX rates are copied manually

- one person understands the consolidation workbook

- reporting is delayed because formatting and reconciliation take too long

- department mappings depend on offline files

At this point, the close bottleneck is no longer only accounting effort.

It is the lack of a clean consolidation and reporting layer above the underlying systems.

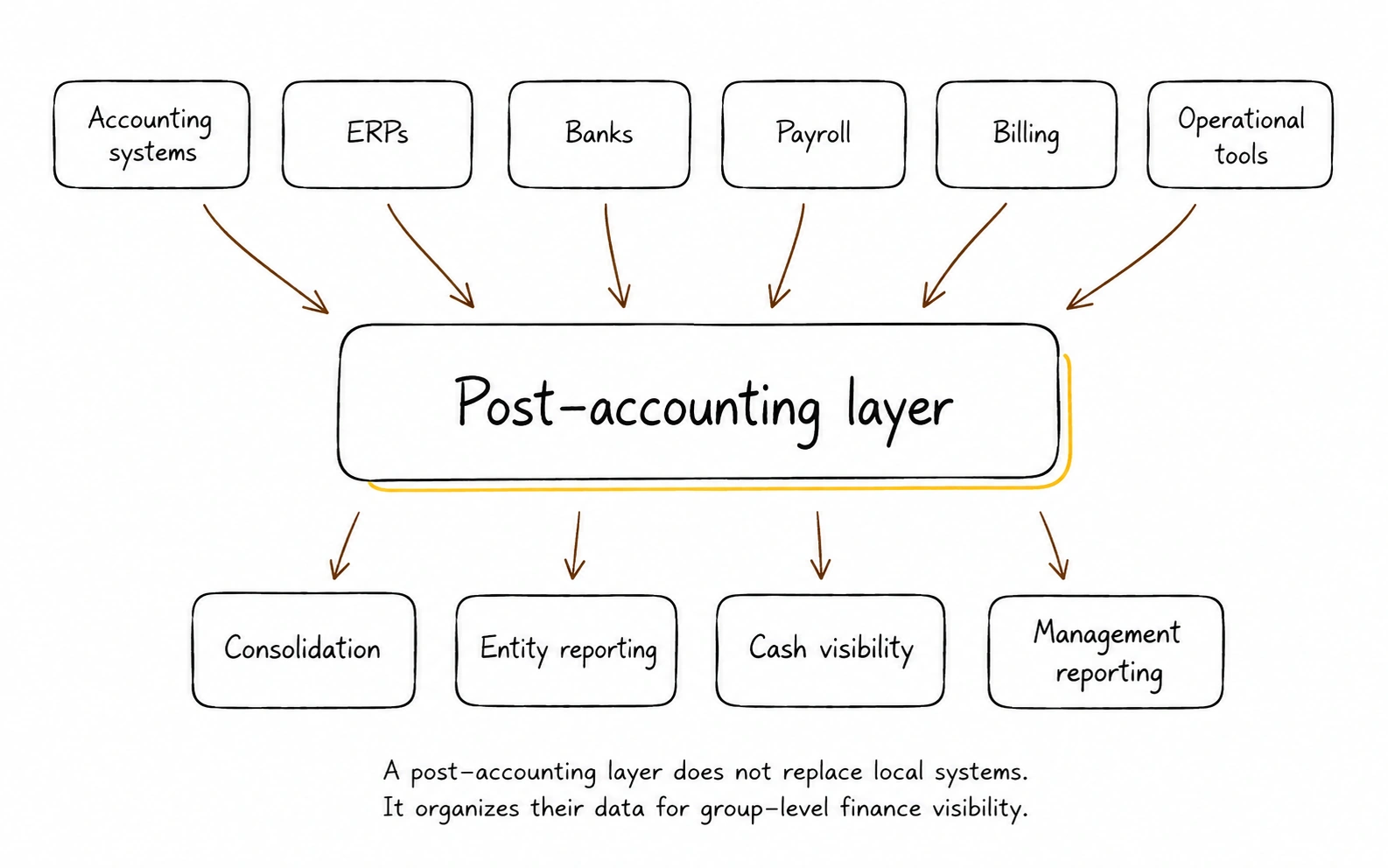

Where a Post-Accounting Layer Fits

A post-accounting layer sits above the accounting systems, ERPs, banks, payroll tools, billing systems, and operational systems a business already uses.

It does not replace those systems. It helps finance teams standardize, consolidate, and analyze the data they need after accounting is complete.

For a multi-entity close process, that means finance can connect local systems, standardize account mappings, support intercompany matching, consolidate entities, improve cash visibility, and produce management reporting faster.

This is where Kudwa fits.

Kudwa helps finance teams turn fragmented accounting, banking, and operational data into clearer consolidation, reporting, and finance analysis without replacing the systems they already use.

For teams closing five, ten or more entities, the reporting delay is rarely caused by one missing report. It's caused by the manual work between local accounting records and the group view leadership needs.

Final Diagnostic: Is Your Multi-Entity Close Process Breaking?

Your financial close process may be outgrowing its current structure if:

- the parent company closes before the subsidiaries are ready

- trial balances need manual reformatting every month

- intercompany balances are reviewed late in the close

- entity-level charts of accounts do not map cleanly

- FX adjustments are handled manually in spreadsheets

- the consolidated pack depends on one fragile workbook

- leadership receives group reporting after the numbers are already stale

- finance spends more time preparing the pack than explaining performance

- entity-level issues are hidden inside the consolidated result

- department-level reporting depends on manual allocation files

- department-level performance can't be consistently compared across entities

If several of these are true, the close process is not just busy. It is structurally overloaded.

Conclusion

A financial close process for multiple entities does not scale in a straight line.

One entity is a ledger close. Three entities introduce mapping, merging, and intercompany pressure. Five entities create a different operating problem: parallel closes, matrix reconciliation, multiple systems, FX translation, and group reporting delays. Beyond five, the problem compounds again as departments, business units, currencies, and reporting dimensions multiply the number of views finance has to reconcile.

The solution is not always more headcount.

Finance teams need a cleaner structure for standardizing entity data, resolving intercompany earlier, consolidating group results, and producing reporting that leadership can use.

If your team is still exporting trial balances into offline spreadsheets, manually mapping accounts, and rebuilding the consolidated view every month, the close process has likely outgrown its architecture.

See how Kudwa helps finance teams standardize entity data, automate consolidation, and reduce manual close bottlenecks.

Latest from Kudwa

Finance KPI Reporting: Why Leadership Teams Disagree on the Same Number

Finance KPI reporting needs controlled definitions, source data, calculation logic, and cadence so leaders stop debating versions of the same metric.

Reporting Software for Finance Leaders: What to Actually Look For

Reporting software for finance leaders should help explain, trace, and defend numbers, not only format dashboards and board packs.