The Multi-Entity Management Reporting Pack: What Finance Teams Should Actually Include

What a multi-entity management reporting pack should include to show group performance, cash, variance, and decisions clearly.

The Pack Is Complete, but the Questions Still Start

It is day eight of the month.

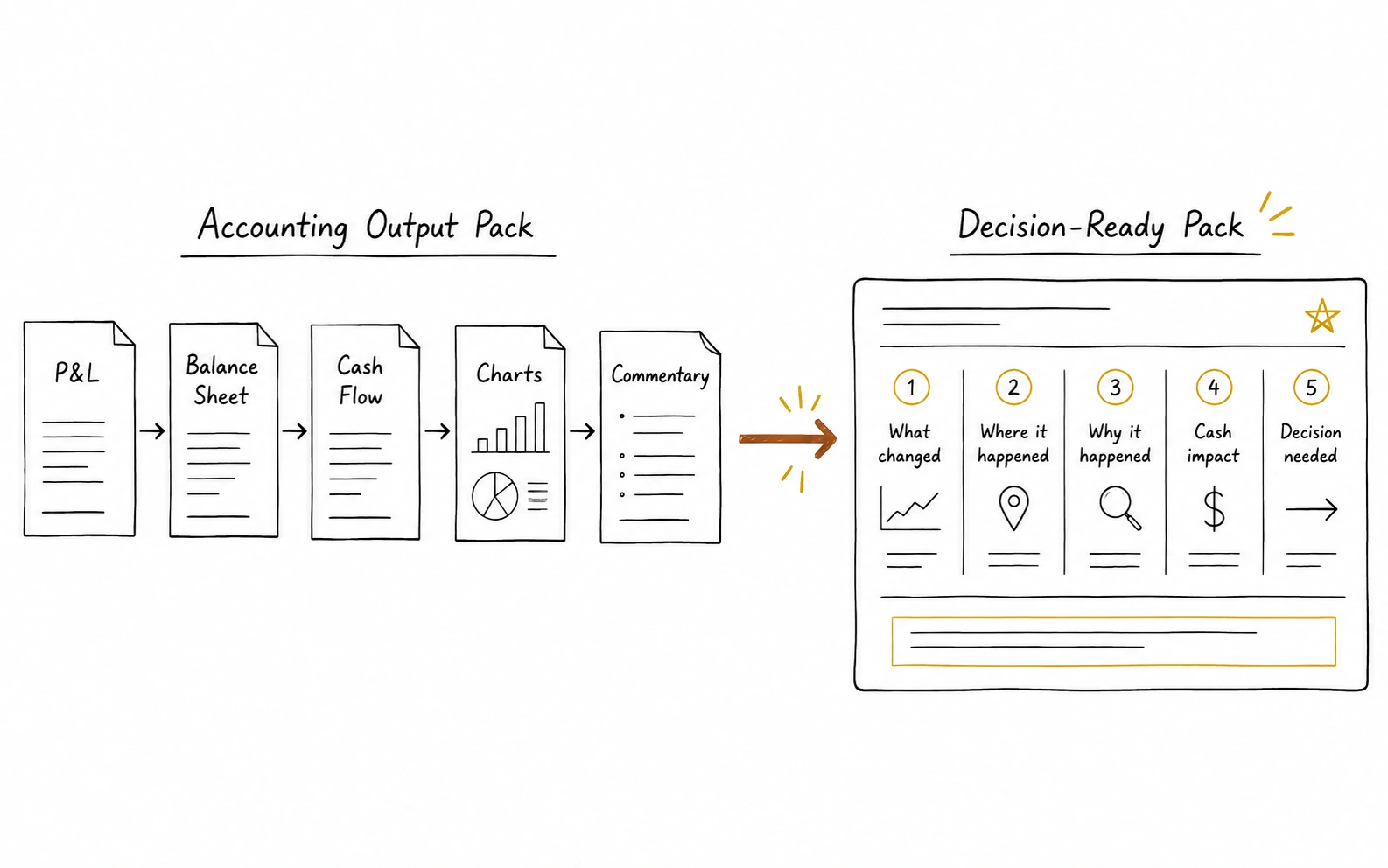

The finance team has closed the books, completed reconciliations, checked the accounting entries, and sent leadership the monthly pack. It includes the P&L, balance sheet, cash flow statement, a few charts, and some commentary.

The numbers are accurate.

Then the questions start.

Why did the UAE entity’s costs rise?

Which business unit is pulling down group margin?

Is the cash movement linked to collections, payments, FX, or timing?

What changed against forecast?

What decision does leadership need to make this month?

This is where many reporting packs fall short.

A multi-entity management reporting pack finance teams can rely on is not just a collection of financial statements. It is a decision sequence. It should show group performance, expose entity-level exceptions, explain cash movement, isolate variance drivers, and make the next decision clear.

Most Reporting Packs Are Built Around Accounting Outputs

Financial statements are necessary. They are not enough.

Most monthly packs are still structured around what finance has closed:

- P&L

- balance sheet

- cash flow statement

- trial balance exports

- budget versus actuals

- charts copied into slides

- short commentary added at the end

That structure makes sense from an accounting perspective. But leadership does not review the business in the same order as an accounting close.

Leadership usually wants to move through a decision sequence:

- What changed?

- Where did it happen?

- Why did it happen?

- Is it cash, margin, timing, or structure?

- What decision is needed?

A good multi-entity management reporting pack follows that sequence.

It does not force leadership to interpret a static set of reports. It guides them from performance to explanation to action.

What a Multi-Entity Management Reporting Pack Should Include

A multi-entity business needs both the group view and the entity-level view. The consolidated picture matters, but so do the exceptions hidden underneath it.

A practical management reporting pack should include these sections:

Executive summary

Leadership question answered: What changed this month, and what needs attention?

Why it matters: Gives leadership a clear starting point before they enter the detail. It should highlight major movements, risks, and decisions.

Consolidated P&L

Leadership question answered: How did the group perform overall?

Why it matters: Shows revenue, margin, cost, and profitability at group level. This is the main performance view, but it should not stand alone.

Entity performance

Leadership question answered: Which entity, business unit, or geography drove the result?

Why it matters: A strong group result can hide weak local performance. Entity-level reporting helps finance isolate where performance is improving or deteriorating.

Cash bridge

Leadership question answered: What changed in cash, and why?

Why it matters: Profit does not explain liquidity. A cash bridge shows movement across collections, payments, funding, intercompany transfers, FX, and timing.

Variance analysis

Leadership question answered: What moved against budget, forecast, or prior period?

Why it matters: Variance analysis separates meaningful movements from noise. It should identify drivers, not just show red and green numbers.

Forecast view

Leadership question answered: What does this mean for the next period?

Why it matters: Leadership needs to understand whether current performance affects future cash, margin, hiring, investment, or expansion plans.

Risks and exceptions

Leadership question answered: What needs attention before it becomes a larger problem?

Why it matters: Flags issues such as overdue receivables, margin compression, cash pressure, entity losses, intercompany mismatches, or unusual cost movements.

Decisions required

Leadership question answered: What does leadership need to approve, change, or investigate?

Why it matters: Turns the pack from a reporting document into a management tool. Each decision should be linked to the evidence in the report.

This structure gives leadership an answer path instead of leaving them to reconstruct the story from disconnected schedules.

Example: How the Pack Should Explain One Variance

The difference between weak reporting and decision-ready reporting often appears in how the pack explains variance.

A basic pack might say:

OPEX increased 14% against budget.

That is technically useful, but it does not explain what leadership should do with the information.

A stronger management reporting pack would show:

Weak reporting

Decision-ready reporting

OPEX increased 14% against budget.

UAE entity drove 80% of the increase. Half came from an annual software renewal, 30% came from approved headcount additions, and the remaining 20% requires review.

Gross margin declined this month.

Group margin fell because one business unit absorbed higher delivery costs. The other entities remained in line with forecast.

Cash decreased during the period.

Cash declined mainly because collections were delayed in one entity, while supplier payments and payroll remained on schedule.

This is the standard the pack should meet. It should not only show that something moved. It should explain whether the movement is timing, structure, performance, or risk.

Why Multi-Entity Management Reporting Breaks

Multi-entity management reporting becomes difficult because the finance team is not only reporting more numbers. They are reporting across more structures.

In GCC businesses, this often means multiple legal entities, free zone and mainland structures, regional offices, business units, currencies, bank accounts, and operational systems. The finance team may still be lean, but the reporting burden grows quickly.

The most common breakdowns come from reporting infrastructure, not finance judgment.

1. Inconsistent chart of accounts

One entity may classify costs differently from another. Revenue lines may not map cleanly. Local accounting logic may work for statutory purposes but create problems at group level.

Without standard mapping, consolidated reporting becomes hard to trust.

2. Manual entity roll-ups

If each entity closes separately and group reporting is assembled manually, finance spends too much time copying, mapping, and checking numbers.

That leaves less time for analysis.

3. Weak intercompany handling

Intercompany balances, recharges, loans, and eliminations can distort group reporting if they are not mapped and reconciled properly.

The issue is not only whether the accounting is correct. It is whether leadership can understand the real group position after internal activity is removed.

4. Cash visibility is split

Cash may sit across multiple banks, currencies, and entities. A group P&L may look healthy while one entity has liquidity pressure or trapped cash.

That is why cash visibility should be part of the management reporting pack, not a separate exercise.

5. Operational data is disconnected

Finance may have the numbers, while sales, operations, or payroll teams hold the context. This creates delays when leadership asks why a variance happened.

The pack should connect financial movement to business drivers where possible.

6. Variance explanations arrive too late

Many packs show budget versus actuals, but the explanation is produced after leadership asks for it.

That means the reporting pack is not doing enough analytical work upfront.

7. Spreadsheet version control slows the process

Spreadsheets can still support finance work. But when they become the core reporting infrastructure, errors and version confusion become harder to avoid.

For a multi-entity business, that fragility compounds every month.

A Better Pack Follows the Decision Sequence

A strong group management reporting pack should not start with every schedule finance produced during close.

It should start with what leadership needs to understand.

A practical sequence looks like this.

1. Start with the Group Position

Begin with the consolidated result. Show whether the business is ahead, behind, or materially different from the prior period, budget, or forecast.

This should include the few numbers leadership needs first:

- revenue

- gross margin

- EBITDA or operating profit

- cash position

- runway or liquidity view, where relevant

- major movements versus budget or forecast

The executive summary should not be a long narrative. It should make the main story visible quickly.

2. Move from Group to Entity-Level Reporting

After the group view, the pack should show where the result came from.

This is where entity-level reporting matters.

Leadership should be able to see whether performance was driven by:

- one profitable entity masking losses elsewhere

- a regional entity with margin pressure

- a business unit with unusual cost growth

- FX movement in one jurisdiction

- delayed collections in a specific entity

- intercompany activity affecting the consolidated view

The goal is not to overwhelm leadership with every entity detail. The goal is to expose the exceptions that matter.

3. Explain Cash Movement Separately from Profit

Cash deserves its own section.

A consolidated P&L can show profit while cash declines. A cash flow statement may exist, but it is often not presented in a way that answers leadership’s practical questions.

A useful cash bridge should explain:

- opening cash

- customer collections

- supplier payments

- payroll

- tax or compliance payments

- debt or funding movement

- intercompany transfers

- FX impact

- closing cash

For multi-entity businesses, cash visibility should also show where cash sits. Group cash is less useful if leadership cannot see which entity controls it.

4. Isolate the Real Variance Drivers

Variance analysis should not only show movement. It should explain the driver.

For example:

- Did revenue increase because of volume, price, timing, or one-off billing?

- Did gross margin fall because of cost inflation, discounting, product mix, or operational inefficiency?

- Did OPEX increase because of hiring, delayed invoices, annual renewals, or structural cost growth?

- Did cash decline because of collections delay, supplier timing, tax payments, or investment activity?

This distinction matters because different drivers require different decisions.

A timing variance may need monitoring.

A structural margin issue needs action.

A cash collection issue may need escalation.

A forecast miss may require plan changes.

5. End with Decisions Required

The final section should make the next step explicit.

This may include decisions such as:

- approve additional hiring

- reduce discretionary spend

- investigate an entity-level margin issue

- revise forecast assumptions

- move cash between entities

- address overdue collections

- review intercompany balances

- delay or accelerate expansion spending

A management reporting pack is decision-ready when it leads to a management conversation, not another reporting request.

What to Systematize, and What Finance Should Still Own

Better reporting is not about removing finance judgment. It is about reducing the mechanical work that prevents finance from using that judgment.

In many teams, too much time goes into preparing the pack and not enough into explaining it.

Systemize the Mechanical Layer

Finance reporting automation should reduce manual work around:

- data pulls from accounting systems, ERPs, banks, payroll, and operational tools

- chart of accounts mapping

- repeatable consolidation rules and checks

- entity roll-ups

- intercompany matching and elimination support

- recurring reporting templates

- cash visibility across entities and banks

- first-pass variance flags

- repeatable monthly reporting workflows

These areas are rule-based, recurring, and error-prone when handled manually.

Keep the Judgment with Finance

Finance teams should still own:

- interpretation

- narrative

- risk assessment

- materiality judgment

- board-level explanation

- decision recommendations

- trade-off analysis

- scenario thinking

Automation should not write the management judgment for the team. It should give finance more time and cleaner data to make that judgment useful. Finance should still decide what is material, what needs explanation, what should be escalated, and what action leadership should take.

The best reporting setup reduces manual assembly and improves the quality of human explanation.

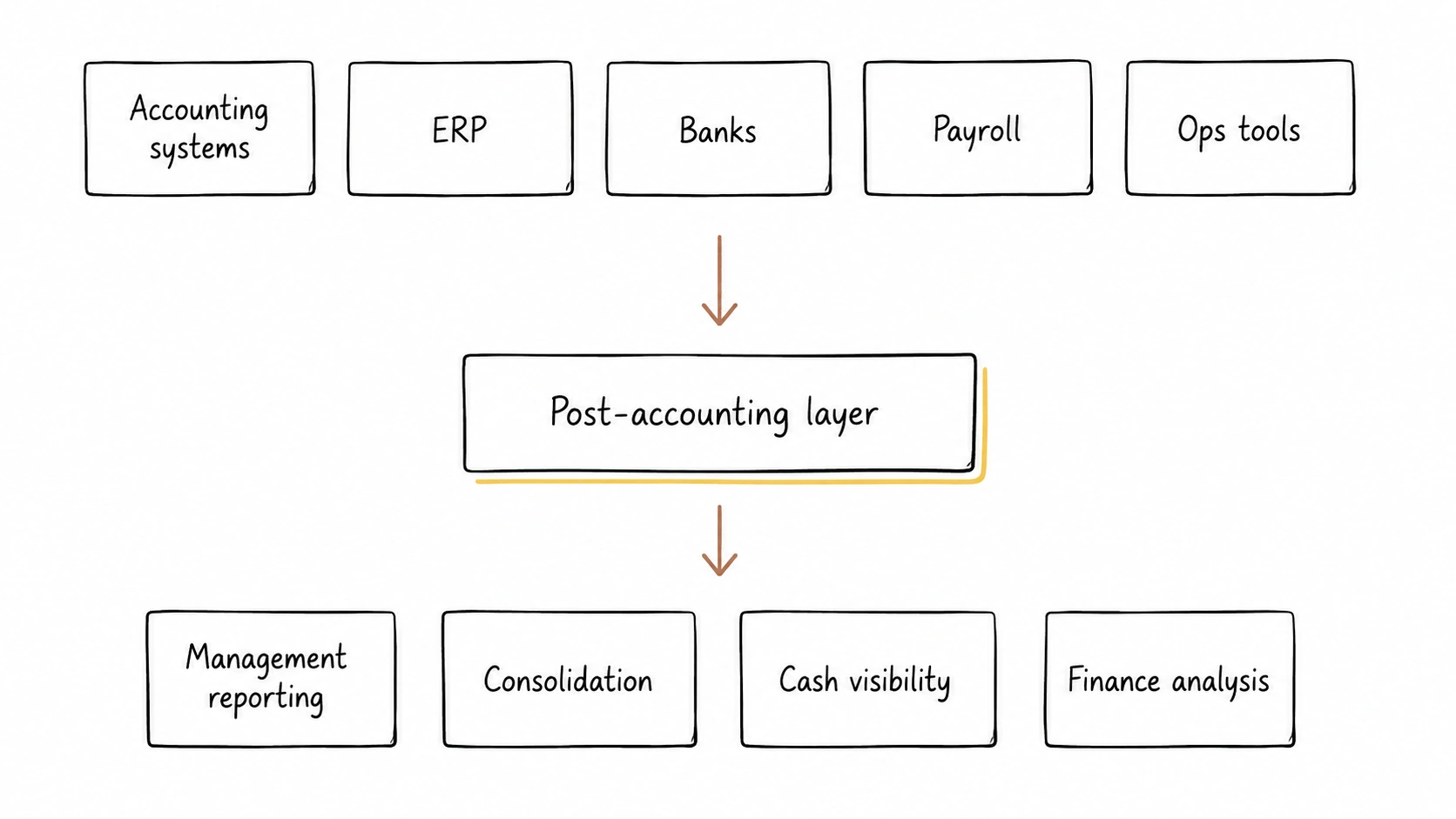

Where a Post-Accounting Layer Fits in Management Reporting

A post-accounting layer sits above the systems a business already uses.

It does not replace the accounting system, ERP, banking platform, payroll tool, or operational systems. Those systems remain important sources of record and workflow.

The post-accounting layer connects and structures the data needed for management reporting.

In practice, that means it helps finance teams:

- standardize data from different systems

- map accounts across entities

- consolidate group reporting

- create entity-level views

- improve cash visibility

- connect financial and operational data

- reduce manual reporting work

- produce repeatable management reporting packs

This is where Kudwa fits. Kudwa helps finance teams turn fragmented accounting, banking, and operational data into repeatable management reporting, consolidated visibility, cash context, and finance analysis...

For multi-entity businesses, this matters because the reporting problem is rarely caused by one missing report. It is usually caused by fragmented systems, inconsistent structures, and too much manual work between close and decision-making.

Your Multi-Entity Management Reporting Pack Is Decision-Ready If…

Your multi-entity management reporting pack is decision-ready if leadership can answer these questions without asking finance to rebuild the report:

- What changed in group performance this month?

- Which entity, business unit, or region drove the change?

- Are the main movements caused by cash, margin, timing, FX, or structure?

- Which variances are material enough to require action?

- Where does cash sit across entities, banks, and currencies?

- What risks or exceptions need leadership attention?

- What has changed against forecast?

- What decision needs to be made before the next reporting cycle?

If leadership still needs finance to rebuild the story after the pack is sent, the issue is not only the format. The reporting structure is not yet decision-ready.

Conclusion

Good management reporting for multi-entity businesses is not about producing a larger monthly pack.

It is about producing a clearer one.

The pack should guide leadership from group performance to entity-level exceptions, from profit to cash movement, from variance to explanation, and from reporting to decisions.

Financial statements remain essential. But they are only one part of the management reporting pack.

For growing GCC businesses with multiple entities, currencies, systems, and lean finance teams, the stronger standard is a reporting pack that answers the management questions before they are asked.

See how Kudwa helps finance teams turn fragmented accounting, banking, and operational data into clearer management reporting.

Book a quick call here.

Latest from Kudwa

Finance KPI Reporting: Why Leadership Teams Disagree on the Same Number

Finance KPI reporting needs controlled definitions, source data, calculation logic, and cadence so leaders stop debating versions of the same metric.

Reporting Software for Finance Leaders: What to Actually Look For

Reporting software for finance leaders should help explain, trace, and defend numbers, not only format dashboards and board packs.