The "Flagship Illusion": Why Your Best Performing Entity Might Be Hiding Your Worst Financial Risks

As GCC groups grow, head offices can hide weak subsidiaries. This blog explains why spreadsheets fail at consolidation, and how to regain group-wide clarity

How to move from intercompany chaos to consolidated clarity in the GCC.

- The "Flagship Illusion": As groups expand, leaders often focus on the main entity's performance while losing visibility into subsidiaries, creating a false sense of financial health.

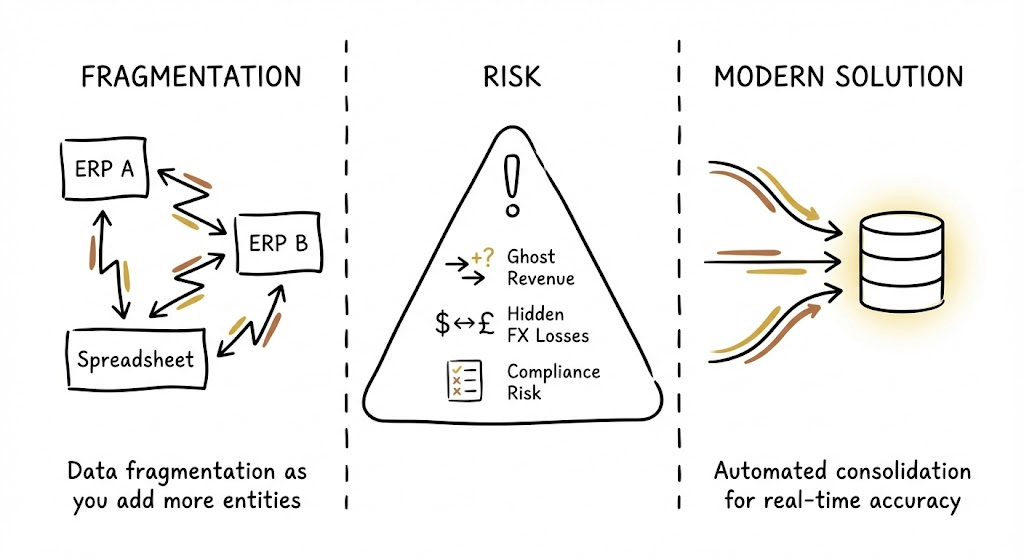

- Data Fragmentation: GCC expansion often results in mismatched systems (e.g., Zoho vs. Wafeq) and inconsistent Charts of Accounts (COA), making manual mapping labor-intensive and inaccurate.

- "Ghost Revenue" Risk: Failing to correctly eliminate intercompany transactions artificially inflates revenue, leading to "growth" that is merely a reporting error.

- Hidden FX Losses: In manual workflows, currency variances and fees are often buried in "adjustment buckets," masking true profitability impact.

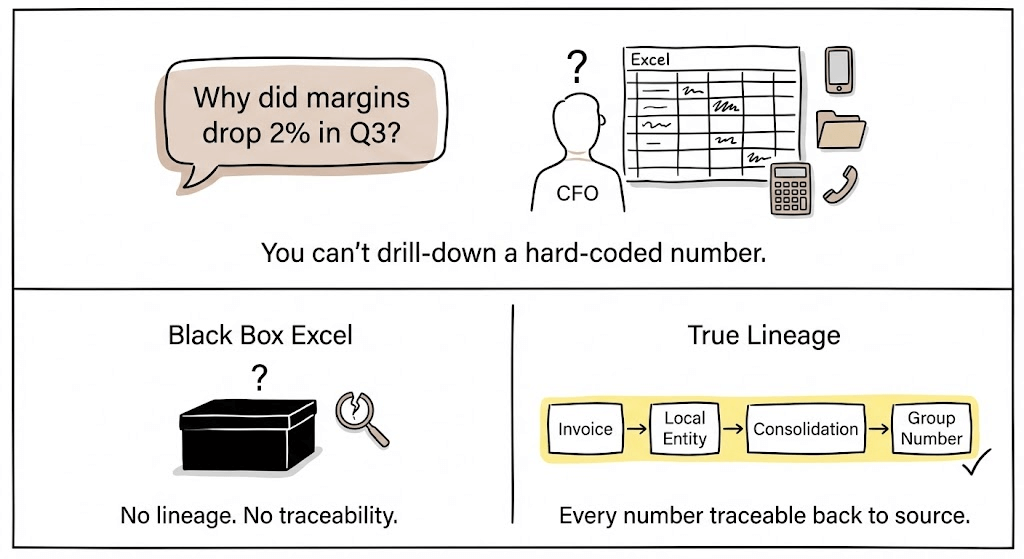

- The "Black Box" Problem: Manual consolidation destroys data lineage. Without "drill-down" capabilities, CFOs cannot verify consolidated numbers against original local invoices.

- Regulatory Compliance Trap: With new UAE Corporate Tax (9%) and Transfer Pricing rules, manual spreadsheet adjustments lack the digital audit trail required by tax authorities.

- The Excel Ceiling: Excel is a calculator, not a database. It lacks the audit controls, scalability, and error-proofing required for multi-entity management.

- The Solution: Automating the consolidation layer provides a "Single Source of Truth," ensuring unified structures, instant eliminations, and complete audit readiness.

The GCC market is moving fast. You open a branch in Riyadh to capture the RHQ benefit. You set up a warehouse in Oman. On paper, the group is growing.

But as you add entities, you lose visibility. In a single-entity business, your bank balance roughly matches your P&L. In a multi-entity group, that link breaks. The danger is that you stop managing the group and start managing the "Flagship" company, which appears to represent the whole picture.

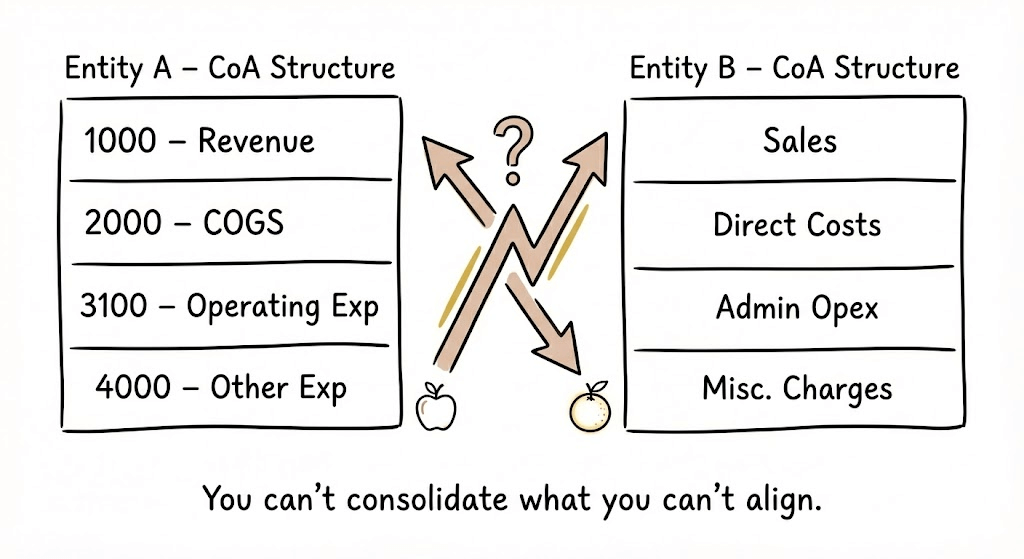

1. The "Apples to Oranges" Problem (COA Mismatches)

The moment you acquire a competitor in Riyadh or open a subsidiary in Doha, you inherit a data problem.

- The Scenario: Your HQ uses Zoho with a standardized COA. Your new Saudi entity uses Wafeq with a completely different account structure.

- The Manual Fail: Every month, your team spends days manually mapping "Travel Expenses" in Entity A to "Business Development" in Entity B.

- The Consequence: You are forcing data to fit where it doesn't belong. This creates reporting lag and makes year-over-year comparisons nearly impossible. You lose the nuance of where money is actually being spent.

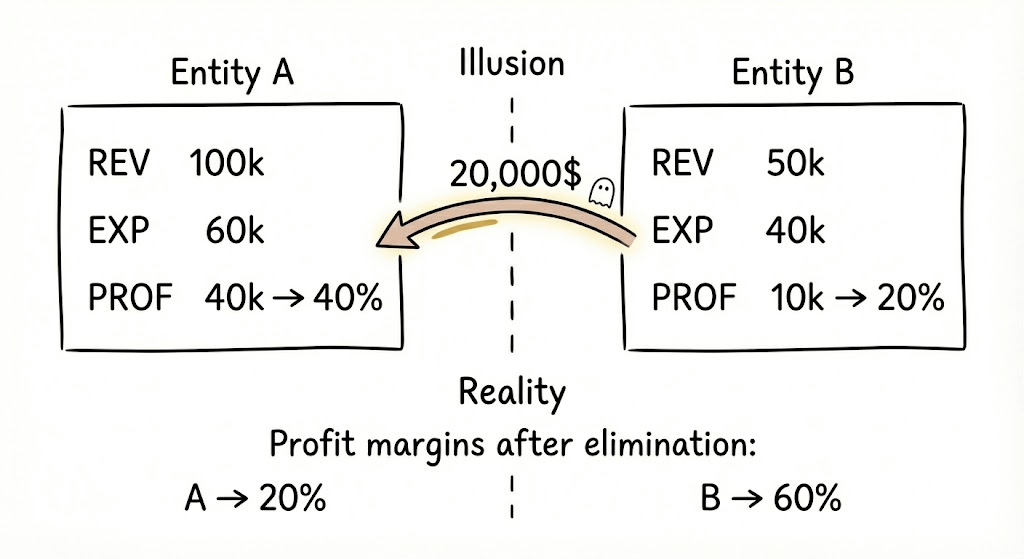

2. "Ghost Revenue" and the FX Fog

Consolidation isn't just addition; it's subtraction.

- The Elimination Headache: If Entity A (UAE) sells to Entity B (KSA), that revenue must disappear from the Group P&L. In Excel, missing just one of these transactions artificially inflates your revenue. You are essentially lying to yourself about your growth.

- The Currency Mask: Even with pegged currencies (AED/SAR), transaction fees and timing differences create variance. In a manual workflow, these variances are often plugged into a "CTA" (Cumulative Translation Adjustment) bucket just to balance the books.

- The Risk: You might be celebrating a 5% revenue jump that is actually just an uneliminated intercompany invoice or a favorable FX swing.

3. The Trust Deficit (Lack of Traceability)

This is the most dangerous moment for a CFO: The Board asks, "Why did margins drop 2% in the Q3 consolidation?" You look at your massive Excel model. You see the hard-coded number. But you cannot click "drill-down." You have to open three different source files, check the formulas, and call the controller in Oman.

Data without lineage is just an opinion. If you cannot trace a consolidated number back to the original invoice in the local entity instantly, you do not have control. You have a "Black Box."

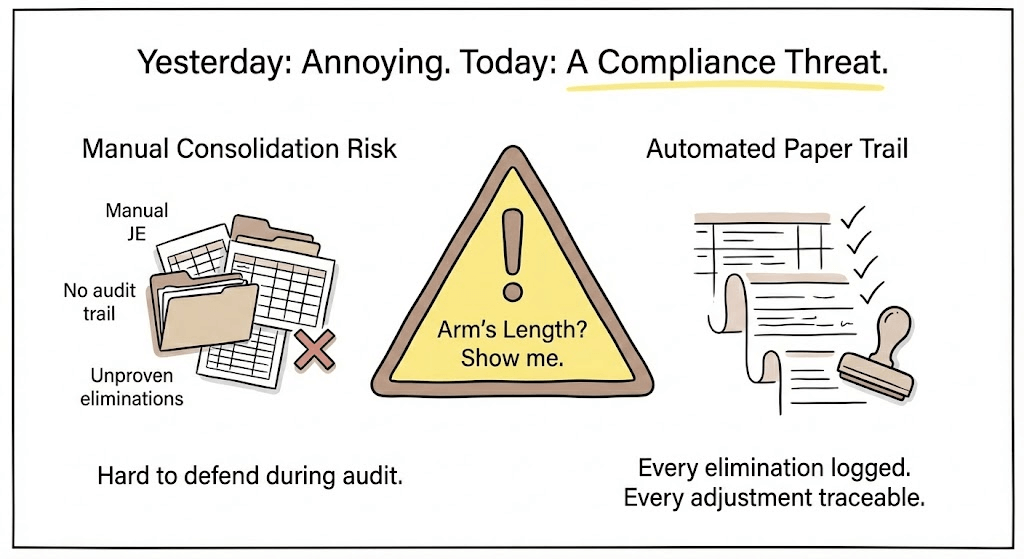

4. The New Threat: The Regulatory Trap

Two years ago, messy consolidation was just an internal annoyance. Today, it is a compliance risk.

- UAE Corporate Tax & Transfer Pricing: With the 9% Corporate Tax, authorities demand to see that intercompany transactions are at "arm's length."

- The Danger: If your consolidations are done via manual journal entries in a spreadsheet, proving the validity of those eliminations during an audit is a nightmare.

- The Shift: You need a system that logs every elimination and adjustment automatically, creating a digital paper trail for the tax man.

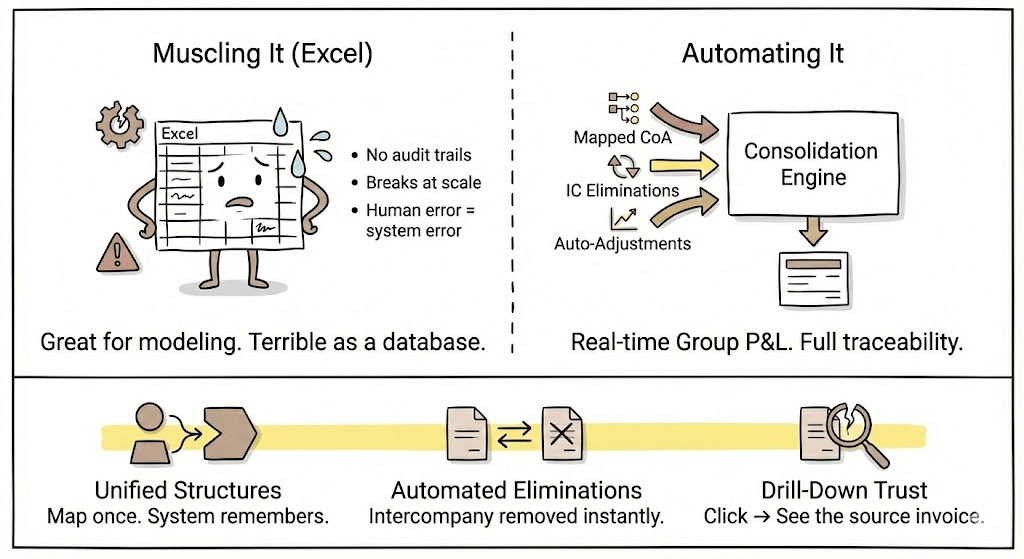

5. Moving from "Muscling It" to Automating It

There comes a point where "working harder" doesn't solve the problem.

- Excel is fantastic for modeling scenarios and ad-hoc analysis. It is the world's best calculator.

- But Excel is a terrible database. It breaks at scale, lacks audit trails, and relies entirely on human perfection.

By automating the consolidation layer, you get:

- Unified Structures: Map different COAs once, and the system remembers.

- Automated Eliminations: The system detects intercompany matches and eliminates them instantly.

- Drill-Down Trust: Click a number on the Group P&L and see the transaction in the local entity.

Summary

You cannot build a regional powerhouse on a foundation of fragile spreadsheets. As your group expands, your tools must mature. It is time to stop spending 80% of your time gathering the data and start spending it analyzing the truth.

Find out more on how to solve these issues. [Book a 15-minute walkthrough]

Latest from Kudwa

Chart of Accounts Standardization Across Entities: Why Consolidation Breaks Without It

Learn how chart of accounts standardization creates consistent mappings, group reporting, and consolidation across multiple entities.

Consolidating Entities You Don’t Fully Own: JV, Local Sponsor, and Minority Interest Reporting in the GCC

Learn how minority interest and JV consolidation affect the group P&L, balance sheet, and monthly reporting workflow across GCC entities.