A Faster Month-End Close Starts Before Day 1

A faster month-end close does not start with more pressure on finance. It starts by moving recurring data dependencies before Day 1.

Executive Summary

- Late inputs: Many close delays start before finance touches the ledger.

- Wrong diagnosis: The issue is not always that finance is slow. Often, the business sends critical inputs too late.

- Pre-close matters: Vendor invoices, payroll changes, revenue data, intercompany balances, and variance context should not first appear after month-end.

- Manual drag: Disconnected systems force finance to collect, clean, and explain data every cycle.

- Entity complexity: Multi-entity businesses add intercompany, FX, consolidation, and reporting dependencies.

- Operating rhythm: A faster close needs clearer ownership before month-end, not just a better Day 1 checklist.

- System layer: Once recurring close work depends on manual exports and spreadsheets, finance needs a cleaner reporting layer above its systems.

The Close Is Not Late Because Finance Is Slow

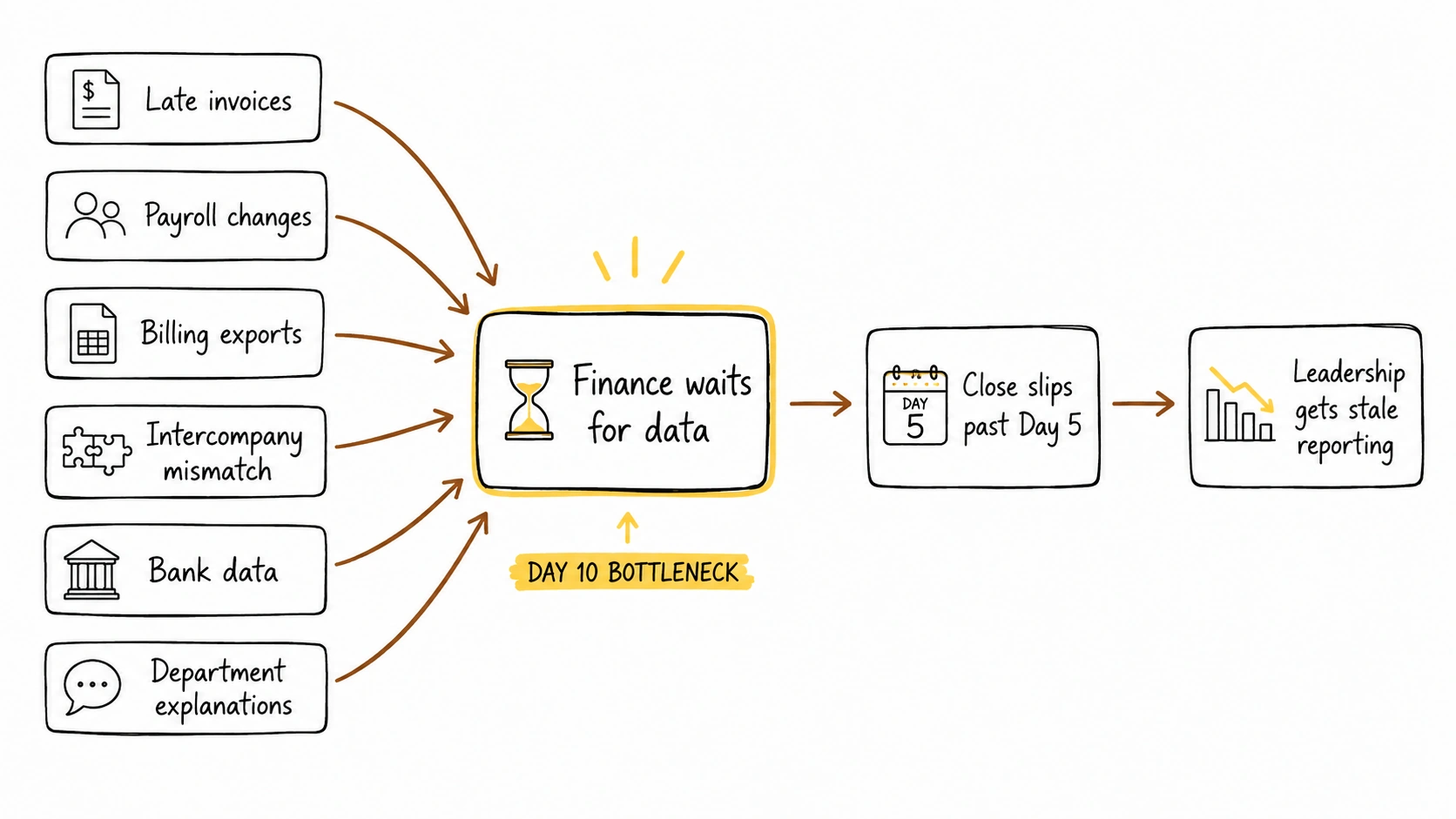

It is 6:00 PM on Day 5. The general ledger is technically locked. Reconciliations are mostly done. The finance team is preparing the actuals vs. budget report.

Then a gap appears.

Software spend is $40,000 lower than expected because the engineering team has not forwarded the final invoice. Payroll needs one more adjustment. One entity has recorded an intercompany recharge, but the other side has not.

The accounting work is not the real issue. The problem is that too much of the close depends on information that arrives after finance needs it.

Most month-end close advice focuses on the trial balance, reconciliations, journal entries, and reporting deadlines. Those steps matter. But they assume the data is already complete.

In practice, the delay usually starts earlier. Finance is still chasing invoices, confirming accruals, reconciling intercompany balances, checking department-level spend, and pulling data from disconnected systems.

A faster close does not start on Day 1. It starts before month-end.

Why the Close Stalls After the Business Scales

At an early stage, month-end close can often be handled by one person with an accounting system, a spreadsheet, and enough context in their head. That changes as the business grows.

Once revenue, transaction volume, entity count, and department ownership increase, the close becomes less about entering numbers and more about collecting, validating, and explaining data from different parts of the business.

This is where the Day 10 bottleneck usually appears.

Finance is not only closing the books. It is waiting for vendor invoices from department heads, payroll adjustments, billing exports, bank and card feeds, revenue recognition inputs, intercompany confirmations, FX adjustments, operational explanations for variances, and missing approvals or supporting documents.

If those inputs arrive late, finance can still close the books. But reporting gets delayed. By the time leadership sees the numbers, the business may already be making decisions on stale information.

This is the historical lag trap: a technically accurate close that arrives too late to guide the next decision.

The Real Fix Is Moving Work Into Pre-Close

The useful question is not only:

How do we close faster after month-end?

It is:

What are we still waiting for after month-end that could have been handled earlier?

That is where many close processes improve. Day 1 should not be spent asking the business for information that could have been collected earlier. It should be spent reviewing, reconciling, posting, and preparing the numbers for reporting.

The rule is simple: if the delay is “waiting for data,” it belongs before Day 1.

That applies to invoices, accrual inputs, intercompany balances, fixed asset updates, payroll changes, revenue data, and department-level explanations. Finance cannot eliminate every late adjustment. There will always be invoices that arrive late, customer issues that need review, and operational changes that happen near the cutoff.

But finance can reduce the number of surprises that appear after the books should already be moving toward close. A faster close is usually built by shifting predictable work earlier.

What Belongs Before Day 1

The pre-close phase should focus on the inputs that repeatedly delay reporting. This does not need to become a heavy process. The goal is to create an operating rhythm where finance is not discovering basic missing information after month-end.

Vendor invoices and accrual inputs

Finance should know which major expenses have been incurred before the final invoices arrive. That means department heads need a clear cutoff for expected invoices, committed costs, and known services received.

If the invoice has not arrived by the cutoff, finance should know whether to accrue it, estimate it based on the contract, or defer it based on policy. Without that discipline, actuals vs. budget analysis becomes misleading. A department may look under budget only because invoices are missing.

Payroll and headcount changes

Payroll is often one of the largest monthly costs. If new joiners, leavers, commissions, bonuses, or one-off adjustments arrive late, both close and variance analysis become harder to trust.

The issue is not only posting payroll correctly. It is explaining why people costs moved. A faster close needs confirmed payroll and headcount inputs before finance starts analyzing actuals.

Revenue and billing data

Billing data should not be reconciled from scratch after the month ends. Finance needs to know whether there were unusual invoices, credit notes, deferred revenue changes, revenue recognition issues, or billing cutoffs that need review.

If the billing system and general ledger do not align, the reporting delay often appears downstream in revenue analysis, cash forecasting, and management reporting.

Intercompany balances

Intercompany should not be discovered during consolidation. For multi-entity businesses, finance should know before close whether “Due To” and “Due From” accounts match, which recharges need to be posted, and whether one side of a transaction has been recorded without the other.

If intercompany issues are left until the consolidated trial balance is under review, the group close turns into a clean-up exercise. A lot of times, intercompany is postponed because of a lack of quick reconciliation. This is where Kudwa shows its value, surfacing intercompany balances from connected accounting systems, helping identify mismatches across entities, and supporting reconciliation before those issues delay consolidation

Department-level explanations

Finance does not control every input. Department heads may own vendor invoices, hiring plans, contract changes, software renewals, or operational metrics.

If ownership is unclear, finance becomes the team chasing everyone else after month-end. A better close process asks department owners for explanations before the reporting pack is already late.

Why Intercompany Should Be Solved Before Consolidation

Intercompany reconciliations are one of the most common reasons a close stretches past Day 7. The issue is not only technical accounting. It is timing.

If intercompany balances are not matched before consolidation starts, finance ends up unpicking the group view after the close is already underway.

For example, Entity A in the UAE pays for a $10,000 global software license. Entity B is supposed to pick up 50% of that cost. If Entity A records the full $10,000 as an expense and Entity B records nothing, the group view becomes distorted. The expense sits in the wrong place, entity-level profitability is misleading, and the reporting pack may require a late adjustment.

A high-performing month-end close process treats the intercompany check as pre-close work, not a late consolidation clean-up.

Before consolidation begins, finance should already know:

- which entities have intercompany balances

- whether “Due To” and “Due From” accounts match

- which recharges need to be posted

- whether loans, shared costs, or management fees are properly recorded

- whether any entity has recorded one side of a transaction without the other

This reduces rework during consolidation and gives leadership a cleaner view of entity-level performance.

Where Manual Close Processes Break

Manual close processes can work for a simple business. They become fragile when the business adds more entities, higher transaction volume, multiple systems, or more reporting pressure.

The breaking point usually appears in four places.

1. Multiple currencies

FX gains, losses, and revaluation adjustments become harder to manage manually as the business adds more currencies, bank accounts, or cross-border entities.

Even when the accounting is correct, leadership still needs a clear explanation of how FX affected cash, margin, or entity-level performance. That explanation is difficult when the rates, calculations, and commentary live across different spreadsheets.

2. Fragmented systems

Billing data may live in one system, payroll in another, bank data in another, and accounting records somewhere else. If finance has to export, clean, and match that data every month, reporting speed depends on manual work rather than a repeatable process.

This is often where the close becomes a reporting problem, not just an accounting problem. The books may be closed, but the numbers are not yet ready for management.

3. Entity complexity

With one entity, the close can often be reviewed in a single accounting file. With multiple entities, finance has to manage mappings, eliminations, intercompany balances, entity-level reporting, and group-level consolidation.

Every new entity adds another layer of review. It also increases the number of relationships finance has to reconcile before leadership can trust the group view.

4. Department-level ownership

As companies scale, finance becomes more dependent on non-finance teams. Department heads may own the context behind spend, hiring, vendor commitments, or operational performance.

If that context arrives late, finance can still produce reports. But those reports will not answer leadership’s next question. A close process is weak when the pack is finished, but the story behind the numbers still has to be rebuilt.

The harder part is quick validation. When a department-level number moves, finance needs to know whether the issue is real, entity-specific, system-specific, owner-specific, or just a mapping problem. This is where Kudwa helps; sitting above the underlying systems. Finance can look at department-level segmentation across different software, entities, and users, then validate the issue without rebuilding the analysis manually.

Where Process Discipline Ends and Systems Need to Help

A faster close is not only a software problem. Some delays require process discipline. Others require better systems. The mistake is treating every delay the same way.

Finance should keep process ownership around:

- invoice submission cutoffs

- accrual policies

- department head confirmations

- approval workflows

- materiality thresholds

- variance explanation ownership

- close calendar accountability

If an invoice arrives late because the business ignored the cutoff, automation alone will not fix the problem. Finance needs a stronger operating rhythm.

But other parts of the close should not depend on manual exports and spreadsheet rebuilding every month. Finance should systematize recurring work around:

- data exports from accounting systems, ERPs, billing tools, and banks

- chart of accounts mapping

- entity roll-ups

- intercompany matching support

- consolidation logic

- recurring reporting templates

- cash visibility across entities and accounts

- first-pass variance flagging

- management reporting pack preparation

These areas are recurring, rules-based, and error-prone when handled manually. At this stage, the issue is no longer just checklist discipline. Finance also needs a cleaner reporting layer above the systems where the data originates.

This is where Kudwa fits. Kudwa helps finance teams connect fragmented accounting, banking, and operational data into a clearer reporting layer, so they can reduce manual exports, improve consolidation visibility, and produce management reporting faster without replacing the systems they already use.

How to Move From Day 10 to Day 5

The fastest way to improve the close is to review the last three close cycles and identify the specific task that caused the delay. Do not start with a broad transformation project.

Start with one question:

What were we still waiting for after Day 3?

Then move that dependency earlier.

If the answer was invoices, create a stronger pre-close invoice cutoff. If the answer was department explanations, assign variance ownership before month-end. If the answer was intercompany mismatches, introduce a pre-close intercompany sync. If the answer was billing data, run a revenue and billing check before close starts.

If the answer was spreadsheet preparation, review which reporting outputs should be standardized or systematized.

A better close process is built by moving recurring delays earlier in the cycle.

Final Diagnostic: Is Your Close Running Late, or Starting Too Late?

There are signs that close will be running late, softwares like Kudwa can help identify and negate these signs:

- major vendor invoices are still being chased after month-end – Kudwa gives you full visibility on your status.

- department heads only explain spend after the pack is drafted – Kudwa gives ownership to each of those heads.

- revenue and billing data are first reviewed during close

- payroll and headcount changes arrive after finance starts variance analysis – Through automated variance analyses, Kudwa shows the reason behind those changes.

- intercompany balances are matched during consolidation instead of before it – Consolidation and reconciliation of dues are automated with Kudwa

- cash accounts are reconciled, but group cash visibility is still unclear – Kudwa shows and explains the group cash accounts automatically.

- material variances are explained after leadership asks – Reviews are automated with Kudwa, and differences are explained.

- the management pack requires major manual rebuilding every month – This is automatic with Kudwa.

- leadership receives numbers too late to make timely decisions – Because of the full view you get with Kudwa, leaders have full visibility.

A stronger close process should let finance validate issues quickly by entity, department, system, and owner. That is the layer Kudwa is built to support: not replacing the close process, but giving finance a clearer way to connect the data behind it.

Conclusion

A faster month-end close does not start with more pressure on finance. It starts by moving predictable bottlenecks earlier.

The goal is not to make the close look organized on paper. The goal is to reduce late inputs, prevent avoidable rework, resolve intercompany issues before consolidation, and give leadership useful reporting while the information is still fresh.

For growing finance teams, the close is no longer just an accounting deadline. It is the starting point for management reporting, cash visibility, variance analysis, and better decisions.

If the delay is waiting for data, move it before Day 1. If the delay is manual reporting work, standardize and systematize the layer above your systems.

Book a demo to see how Kudwa helps finance teams reduce manual close bottlenecks and turn fragmented finance data into clearer reporting.

Latest from Kudwa

Finance KPI Reporting: Why Leadership Teams Disagree on the Same Number

Finance KPI reporting needs controlled definitions, source data, calculation logic, and cadence so leaders stop debating versions of the same metric.

Reporting Software for Finance Leaders: What to Actually Look For

Reporting software for finance leaders should help explain, trace, and defend numbers, not only format dashboards and board packs.