Reporting Software for Finance Leaders: What to Check Before You Trust the Board Pack

Reporting software for finance leaders should do more than present charts. It should connect to source data, explain variance, and produce defensible reports.

Executive summary

- Boardroom test: A finance report is only useful if the CFO can defend the number when the follow-up question comes.

- Presentation gap: Many reporting tools show the variance but cannot explain what caused it.

- Traceability need: Finance leaders need to move from group total to entity, account, department, vendor, customer, or transaction without rebuilding the report.

- Accuracy risk: Reports built from manual extracts may look polished while still carrying uncertainty from the preparation process.

- Context layer: The difference between a dashboard and a board-ready report is source context, variance explanation, and consolidated accuracy.

- System requirement: Reporting software should connect to underlying data, preserve logic, and keep figures defensible.

- Practical test: If the tool produces visuals the finance leader cannot defend under questioning, it is a presentation layer, not a reporting system.

A CFO presents the quarterly numbers.

Marketing spend is up 18% against plan.

The dashboard shows the 18%. The board pack shows the 18%. The chart is clean. The number is accurate.

Then a board member asks:

Why?

The room pauses.

Was it campaign timing? Agency fees? A one-off brand project? Spend in one entity? A reclass from sales? A late invoice? FX? Something booked in the wrong period?

The reporting tool cannot answer. It only shows the variance.

The CFO promises to come back with the detail, which means another two days of digging through accounting exports, department files, invoices, and budget schedules.

The reporting tool produced a number.

It did not produce an answer.

That is the standard finance leaders should use when evaluating reporting software for finance leaders. The question is not whether the tool can present data cleanly. Most tools can. The question is whether the report can survive the follow-up question.

Reporting software for finance leaders should be judged by answerability

Finance leaders do not need reports only to display numbers.

They need reports to support decisions.

That means the report must do three things at the same time:

- show the number clearly

- explain the movement behind it

- prove where the number came from

If one of those is missing, the report is incomplete.

A dashboard that shows group margin dropped by 3 points may be visually correct. But if the CFO cannot drill into which entity, product line, customer mix, cost category, or transaction drove the movement, the report has stopped too early.

A board pack that shows cash decreased may be accurate. But if finance cannot explain whether the movement came from delayed collections, payroll timing, supplier payments, intercompany transfers, restricted cash, or FX, the number is not decision-ready.

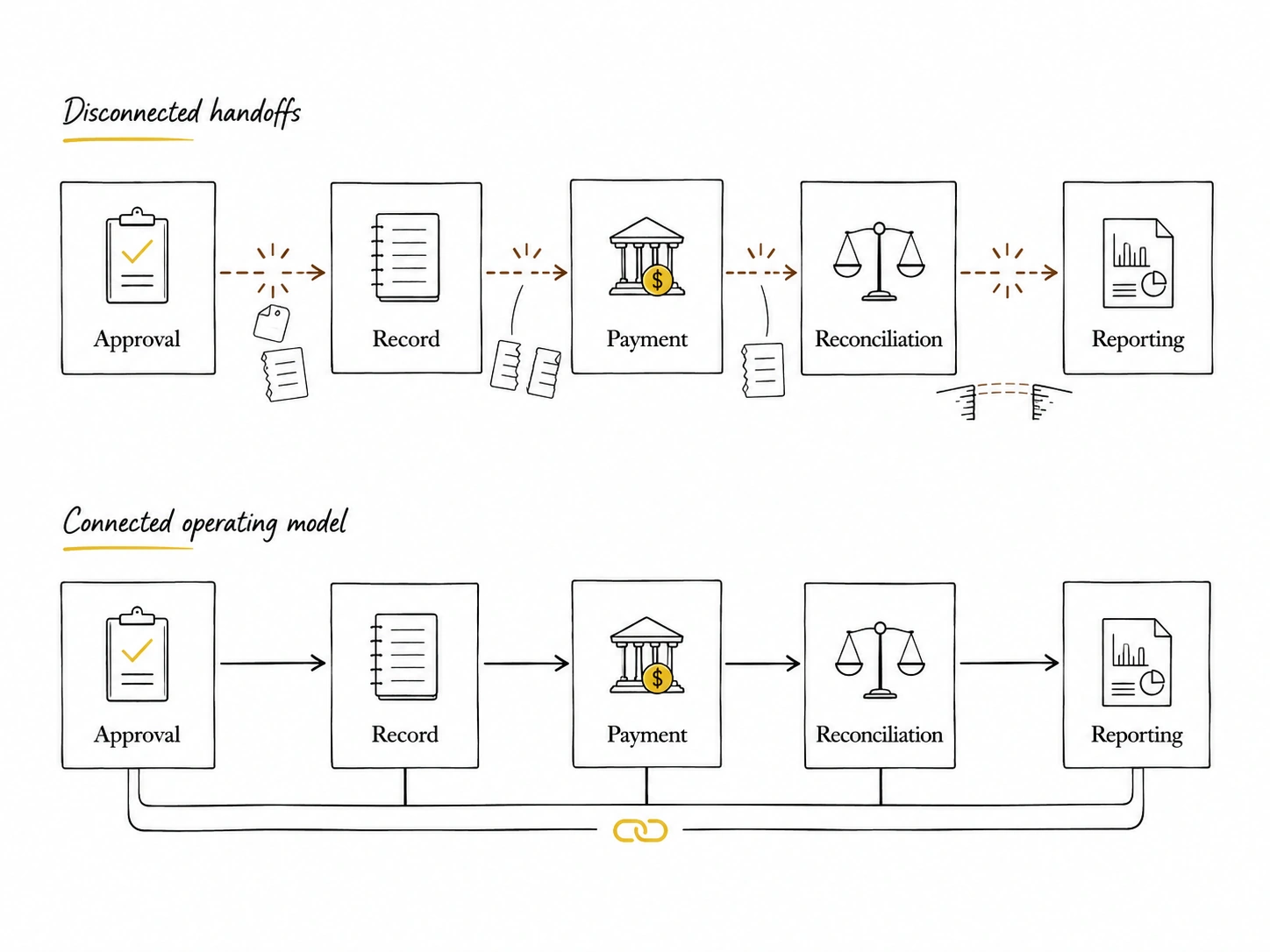

This is the difference between reporting as presentation and reporting as finance infrastructure.

Presentation answers: what changed?

Finance reporting answers: what changed, why did it change, where did the number come from, and what should we do next?

That is the standard a finance leader should expect.

The gap between a dashboard and a report a CFO can defend

A dashboard can be useful.

It can make trends visible. It can reduce time spent formatting. It can help teams compare performance across periods, entities, departments, or KPIs.

But a dashboard becomes weak when it is treated as the final answer.

For a CFO, the report is not finished when the chart is produced. It is finished when the figure can be defended.

That requires context.

A defensible report needs:

The report supports follow-up questions in the room, not after two days of offline work

This is the real buyer criteria.

If reporting software cannot support those jobs, it may still be useful. But finance should call it what it is: presentation, not full reporting.

Where reporting tools usually stop too early

Most reporting tools fail in the same place.

They show the output without carrying the operating context behind it.

That can happen even when the chart is correct.

A report shows revenue by entity. But the revenue data came from a manually assembled extract.

A report shows EBITDA movement. But finance cannot see which cost categories drove the variance without opening the accounting export.

A report shows group cash. But bank balances, uncleared payments, restricted funds, and intercompany transfers were adjusted in a spreadsheet before upload.

A report shows marketing spend up 18%. But campaign, vendor, department, and invoice-level context live outside the reporting layer.

The tool may not be wrong.

It may be downstream of the real problem.

If the reporting software receives a flat file that has already been summarised, cleaned, and stripped of source detail, it cannot answer deeper questions later.

It can only report what it was given.

That is why finance leaders should evaluate the data path behind the report, not only the report itself.

The failure mechanism: reporting that presents without explaining

Take a group margin example.

A board pack shows that group gross margin dropped from 42% to 39%.

The board asks which entity drove the decline.

The reporting tool cannot drill into the entity level because the dashboard was fed a summarised, manually assembled extract. The finance team had rolled the numbers into a clean group view before uploading them.

The group number is accurate.

But the path behind it is gone.

To answer the board, finance needs to reopen the original entity reports, check revenue mix, review cost of sales, compare FX treatment, and see whether one large customer or supplier explains the movement.

The report described the what.

It could not reach the why.

The problem is not only inconvenience. It weakens the CFO’s position in the room.

A finance leader is not judged only by whether the number is correct. They are judged by whether they can explain and defend it while decisions are being made.

This is where reporting quality becomes a leadership issue, not a formatting issue.

Why basic reporting works at first

Early reporting can work with basic tools because the business is simple enough for people to carry the context.

One entity. One accounting system. One bank. One reporting pack. One finance person who knows the details.

In that environment, a dashboard or spreadsheet report may be enough.

If marketing spend increases, the CFO probably knows the campaign. If payroll moves, the finance manager knows the hires. If cash drops, someone remembers the supplier payment.

The report does not need to hold every explanation because the team still holds the context.

That changes as the business grows.

More entities. More bank accounts. More departments. More currencies. More cost centres. More systems. More board-level scrutiny.

The finance leader can no longer rely on memory to defend every number.

The reporting system has to carry more of the context.

Where complexity increases

Reporting becomes harder when the follow-up questions become more specific than the report structure.

Reports need to drill from group to entity to transaction

A group-level P&L is not enough when performance differs by entity.

A CFO needs to move from total marketing spend to UAE entity, KSA entity, department, vendor, invoice, and period.

If the reporting tool only holds the group total, the answer leaves the system immediately.

That is where delays begin.

Variance needs explanation, not display

Variance reporting is not the same as variance explanation.

A report can show that payroll is up 12%.

Finance still needs to know whether the driver is headcount, commissions, bonuses, contractor reclassification, department transfer, employer contributions, or timing.

If explanation requires separate source work, the report is incomplete.

Multiple stakeholders ask different questions of the same report

The CEO asks about cash impact.

The board asks about margin.

The COO asks about department spend.

The investor asks whether variance is recurring.

The same finance report needs to support different levels of questioning.

A static presentation cannot handle that unless the data underneath remains connected.

Finance leaders are held to numbers in real time

Board meetings do not wait for offline reconciliation.

If the CFO cannot answer in the room, confidence weakens. Even when the number is ultimately correct, the delay creates doubt.

That is the risk of reports that look finished but are not explainable.

Reporting cadence shortens

Monthly reporting gives finance time to rebuild.

Weekly or rolling reporting does not.

When leadership expects faster answers, the reporting layer cannot depend on manual extract, clean, upload, review, and explain cycles.

The system has to carry the logic before the question is asked.

GCC example: group reporting across entities and currencies

This issue is common in GCC groups because reporting complexity often arrives before large finance headcount.

A UAE-based group may report to a board across UAE and KSA entities. One entity operates in AED, another in SAR, and group reporting may be prepared in USD.

The quarterly report shows operating expenses up 14% against plan.

The board asks whether the increase came from the UAE entity, the Saudi entity, FX, payroll, rent, or one-off professional fees.

If the reporting software only shows a consolidated OPEX line, the CFO has a problem.

The answer may require:

- entity-level drill-down

- currency impact review

- payroll detail

- vendor-level cost movement

- comparison against budget assumptions

- source invoices or ledger transactions

- intercompany treatment

That is not a generic dashboard issue.

It is a reporting depth issue.

For regional finance leaders, the tool must support entity, currency, and source-level explanation. Otherwise, the report is only board-facing on the surface.

What finance leaders should expect from reporting software

Reporting software for finance leaders should be evaluated on the work it removes from the reporting process and the confidence it creates in the final report.

It should do more than format outputs.

1. Connect to source data rather than receive dead extracts

A report built from a static upload loses context quickly.

The system should connect to accounting, banking, payroll, billing, AR, AP, spreadsheets, and relevant operational data where needed.

This does not mean every source has to be perfectly automated from day one. But the direction should be clear: fewer dead extracts, more connected data.

This is the same underlying requirement discussed in What a Unified Financial Data Platform Actually Replaces in a Growing Finance Stack: the real value is not another report, but a cleaner layer between finance systems and decisions.

2. Preserve drill-down from summary to source

Finance leaders need to move through the report without leaving the reporting logic behind.

A strong reporting system should let the user move from:

- group P&L to entity P&L

- entity variance to department movement

- department movement to account detail

- account detail to vendor, customer, invoice, or transaction

- reported figure to source system

This is not a nice-to-have. It is how finance defends the number.

3. Explain variance, not only flag it

A variance is not an explanation.

If revenue is up 20%, the system should help identify whether the movement came from volume, price, customer mix, timing, entity contribution, new contracts, or one-off recognition.

If payroll is up 12%, the system should help separate headcount, bonuses, commissions, reclassifications, accruals, and timing.

If cash is down, the system should help connect collections, supplier payments, payroll, intercompany, restricted cash, and FX.

This is where finance reporting and analysis should operate together. Reporting shows the figure. Analysis explains the movement.

4. Maintain consolidated accuracy

Consolidated reporting is not just adding numbers together.

A proper reporting layer needs controlled mappings, entity structures, eliminations, currency treatment, account groupings, and reporting definitions.

If those live in spreadsheets outside the system, the board pack may still depend on manual logic no one wants to reopen.

That is where accuracy risk enters.

Not because the finance team is careless, but because the report relies on too many invisible preparation steps.

5. Keep every material figure traceable

Traceability is what separates a defensible report from a polished slide.

Finance should be able to answer:

- Where did this number come from?

- Which source system produced it?

- What mapping was applied?

- What period does it belong to?

- Was it adjusted?

- Who changed it?

- Can we see the underlying detail?

Without traceability, the report depends on trust in the preparer.

With traceability, the report can be challenged and defended.

6. Produce board-ready output without manual rebuilds

A reporting system should not require finance to rebuild the same pack every cycle.

Recurring board reports, management packs, variance summaries, and cash views should be produced from controlled structures.

Finance should review and explain the report, not recreate its base.

This matters especially for lean teams. When reporting quality depends on repeated manual effort, small teams lose the time they need for analysis. That connects directly to How Lean Finance Teams Can Run Serious Reporting Without Adding Headcount.

Buyer checklist: is this reporting software or presentation software?

Finance leaders should test reporting tools against the boardroom follow-up question.

Use this checklist.

The last question is the most important.

If the report fails when someone asks “why,” the tool has not solved the finance leader’s reporting problem.

It has only improved the presentation of the problem.

Where software becomes necessary

A stronger reporting model becomes necessary when the report needs to carry context and traceability, not just presentation.

That point usually arrives when:

- leadership asks follow-up questions faster than finance can rebuild the detail

- reports need to move from group to entity to transaction

- variance explanation becomes part of the reporting expectation

- consolidated accuracy depends on manual files

- multiple stakeholders need to trust the same report

- board packs need to be produced repeatedly without rework

- finance leaders are expected to defend numbers in real time

At that stage, reporting software should not be judged by how the dashboard looks.

It should be judged by how far the report can go before finance has to leave the system.

This is where a post-accounting layer such as Kudwa can help: not by replacing the accounting system or creating prettier charts, but by connecting finance data, preserving traceability, and supporting reporting that finance leaders can defend.

The practical takeaway is simple.

A report is not board-ready because it looks polished. It is board-ready when the CFO can answer the next question without rebuilding the number offline.

Latest from Kudwa

Chart of Accounts Standardization Across Entities: Why Consolidation Breaks Without It

Learn how chart of accounts standardization creates consistent mappings, group reporting, and consolidation across multiple entities.

Consolidating Entities You Don’t Fully Own: JV, Local Sponsor, and Minority Interest Reporting in the GCC

Learn how minority interest and JV consolidation affect the group P&L, balance sheet, and monthly reporting workflow across GCC entities.